Monday, May 18, 2026

NAR Existing-Home Sales Report Shows 0.2% Increase in April

NAR Existing-Home Sales Report Shows 0.2% Increase in April: Month-over-month sales increased in the Midwest and the South, were unchanged in the Northeast, and declined in the West. On a year-over-year basis, sales rose in the South, were flat in the West, and fell in both the Northeast and Midwest.

Monday, May 11, 2026

Could Co-Buying Be the Answer for Some First-Time Buyers?

Could Co-Buying Be the Answer for Some First-Time Buyers?

For a lot of would-be first-time buyers, affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying.

The Dream Is Still Alive. The Math Just Isn’t Working for Everyone.

Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation.

The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981.

But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door.

So, What’s Co-Buying?

Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner.

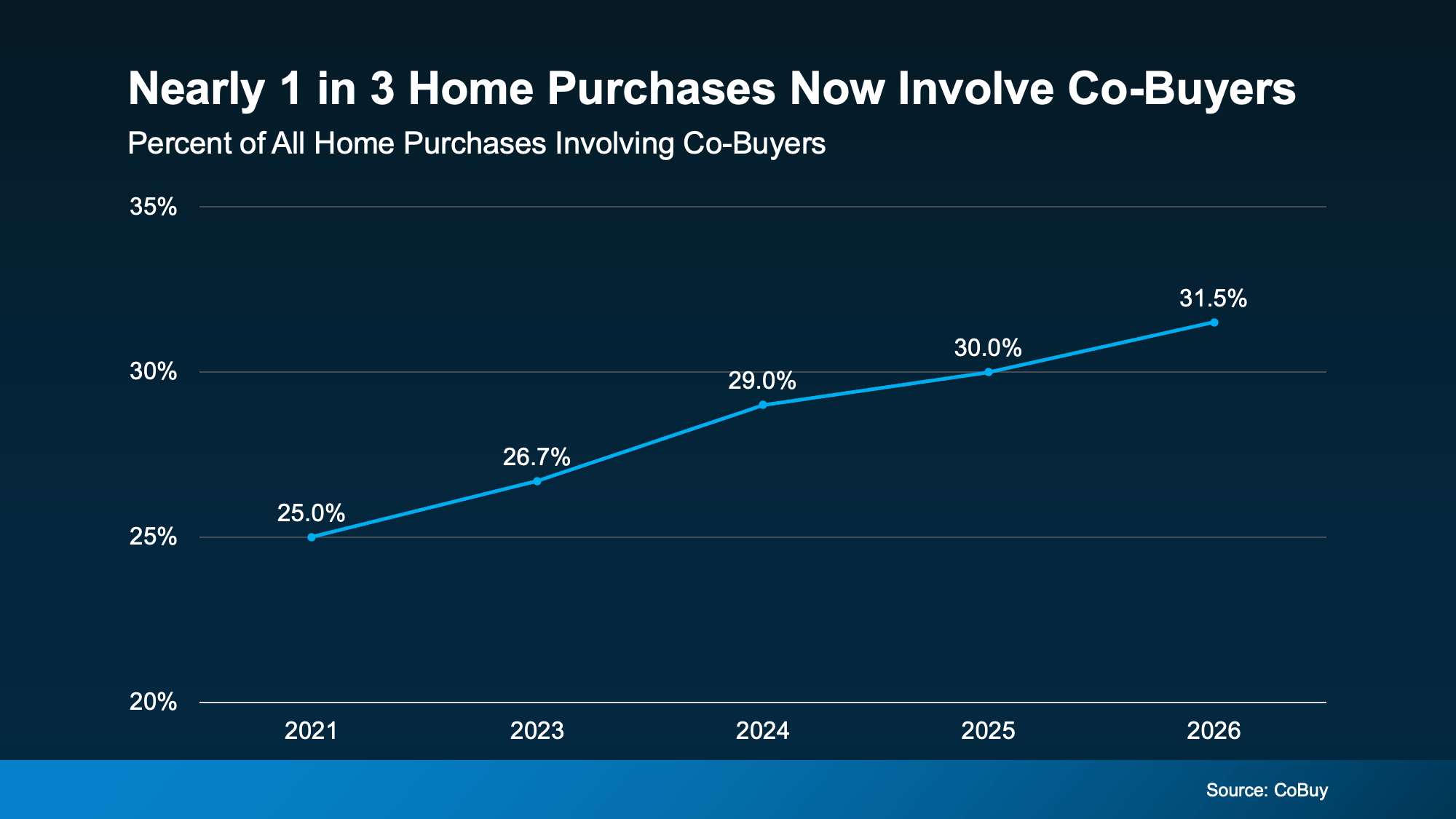

And it's catching on fast, just look at where things stand today. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below):

Why It Works

Why It Works

Here are just a few of the top reasons buyers are going this route, according to NerdWallet:

Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours.

More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own.

Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers.

Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting. Plus, sharing costs can make repairs or renovations more manageable, too.

Things To Keep in Mind

If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road.

That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment.

Bottom Line

Affordability challenges are real, but they don't have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots.

If you're curious whether it could work for your situation, let's talk. Reach out today and let's figure out your path to homeownership together.

Wednesday, May 6, 2026

4 Ways To Give Your Offer an Edge This Spring

4 Ways To Give Your Offer an Edge This Spring

Looking to buy a home this season? Here's what you should know.

Buyers have more leverage today than they’ve had in years. There are more homes to choose from and, in many areas, sellers are more open to negotiation.

But that doesn’t mean competition is gone completely. These days, it varies a lot depending on where you’re hoping to move.

If you’re buying in a popular neighborhood, or in a market where there aren’t many homes for sale, you may still find yourself competing with another buyer.

And that’s especially true in the Spring. Here's how to stay one step ahead of any competition this season.

Why Your Best Offer Still Matters This Spring

According to experts at Zillow and Realtor.com, Spring is one of the busiest times of year to buy a home.

That’s because many buyers want to move now so they can settle in before the next school year. And when more buyers enter the market, competition naturally picks up.

So, depending on where you’re buying, you may still need to move quickly and make a strong offer, even though the market overall has moderated. And that’s especially true if you find a home you really love.

This is what you need to know to make your offer stand out.

1. Lead with a Strong, Realistic Offer

It’s tempting to start low and negotiate up. And in some markets, that strategy can work. But if a home is priced well and getting attention, lowballing could hurt your chances.

Instead, focus on making an offer that reflects your local market. As Bankrate explains:

“There is no magic formula for an optimal home offer. Any offer will be heavily dependent on asking price and local market conditions . . . Your real estate agent will know the local market well and can advise what a competitive — but fair — offer will look like in your area.”

The goal is to make an offer that makes sense for you and stands out to the seller.

2. Have a Plan for Competing Offers

If you’ve fallen in love with a home, it’s important to have a plan in case there’s competition from another buyer. One strategy your agent may discuss with you is an escalation clause, which Investopedia explains like this:

“An escalation clause is a way to automatically escalate your bid by a certain dollar amount, up to a certain ceiling, to compete with other bids.”

The key is knowing your budget and sticking to it. You don’t want to lose out over a small difference – and this can help prevent that. But you also don’t want to overpay.

Keep in mind that if the appraisal comes in lower than your offer, you may have to make up the difference out of pocket. Your agent can help you weigh those risks and determine the best approach for your situation.

3. Keep Your Offer Clean

Price matters. But sellers also look closely at your offer’s terms. In some cases, a simpler, cleaner offer can stand out – even if it’s not the highest. As Redfin says:

“Sellers tend to want clean, straightforward offers with minimal strings attached. Keep your requests simple and focus on the essentials.”

Your agent can help you prioritize what matters most, so you’re not giving up things you need, while still making your offer as appealing as possible.

4. Be Flexible Where You Can

Sometimes, what helps your offer the most is understanding what matters to the seller. NerdWallet explains:

“As you prepare an offer, you tend to focus on what the seller has (a house) and what you want (their house). But you’ll gain a competitive edge by viewing the transaction from the seller’s eyes: What does the seller want?”

Does the seller need extra time to move out? Or do they want to move as soon as possible? Your agent can talk with the seller’s agent to find out what matters most. Flexibility here can make a big difference in how your offer is received.

Bottom Line

Today's market may be balancing out, but strong offers still matter – especially during the busy Spring season.

Curious how competitive things are (and what it’ll take to win) in our market? Let’s talk.

Thursday, April 30, 2026

Is Late May the Best Time To List Your House?

Is Late May the Best Time To List Your House?

You may have heard April 12-18 was the “best week” to list your house. That’s based on a report from Realtor.com. But now that it’s passed, you may be wondering if you missed your moment.

Here's the good news – you didn’t.

Because the reality is, there isn’t just one perfect week to sell your house this Spring. There’s a window. And right now, you’re still in it.

Your Window To Sell Is Still Wide Open

Here’s why. Different organizations run studies like this every year. And they don’t always land on the exact same week. That’s okay. It’s because they're using different research methods and even different definitions of what “best” means.

But the fact that the results vary points to a larger trend. While there may be sweet spots, the entire Spring season gives sellers an opportunity to get some of the best conditions (and best sales prices) of the year.

And it’s definitely not too late to jump in.

Why Listing in Late May Is the Perfect Play

According to Zillow, the best time to list your house this year is the last 2 weeks of May. And that’s approaching fast.

Based on their analysis, this is the ideal time to do it if you want to make top dollar. Because, in this 2-week window, homes sell for more. Sometimes, quite a bit more.

Depending on where you are and the price point in your area, some homeowners may even net tens of thousands of dollars extra in this sweet spot. As Zillow explains:

“Why late spring? Buyer demand typically peaks before Memorial Day. Families want to move during the summer and settle in before the new school year. More buyers shopping at once can spark competition and lift prices.”

And they’re not the only ones saying listing in May could be the key to selling for more. ATTOM Data analyzed almost 52 million home sales over the past 10 years and found sellers in May are achieving some of the highest returns.

That means the ideal window this year is very much still open.

What This Means for You

If your goal is to sell for the strongest possible price, this is where timing and strategy come together. And you want to be sure you’re ready to make the most of it.

So, what should you be doing right now?

When prepping for a fast-moving window like this, you don’t want to waste time or money on the wrong prep work. And your agent is your go-to to make sure you’re focusing on the right things.

They’ll be able to tell you if the “best week” is slightly different in your market. And what quick repairs or updates can help you get a higher price, without taking a ton of time or effort.

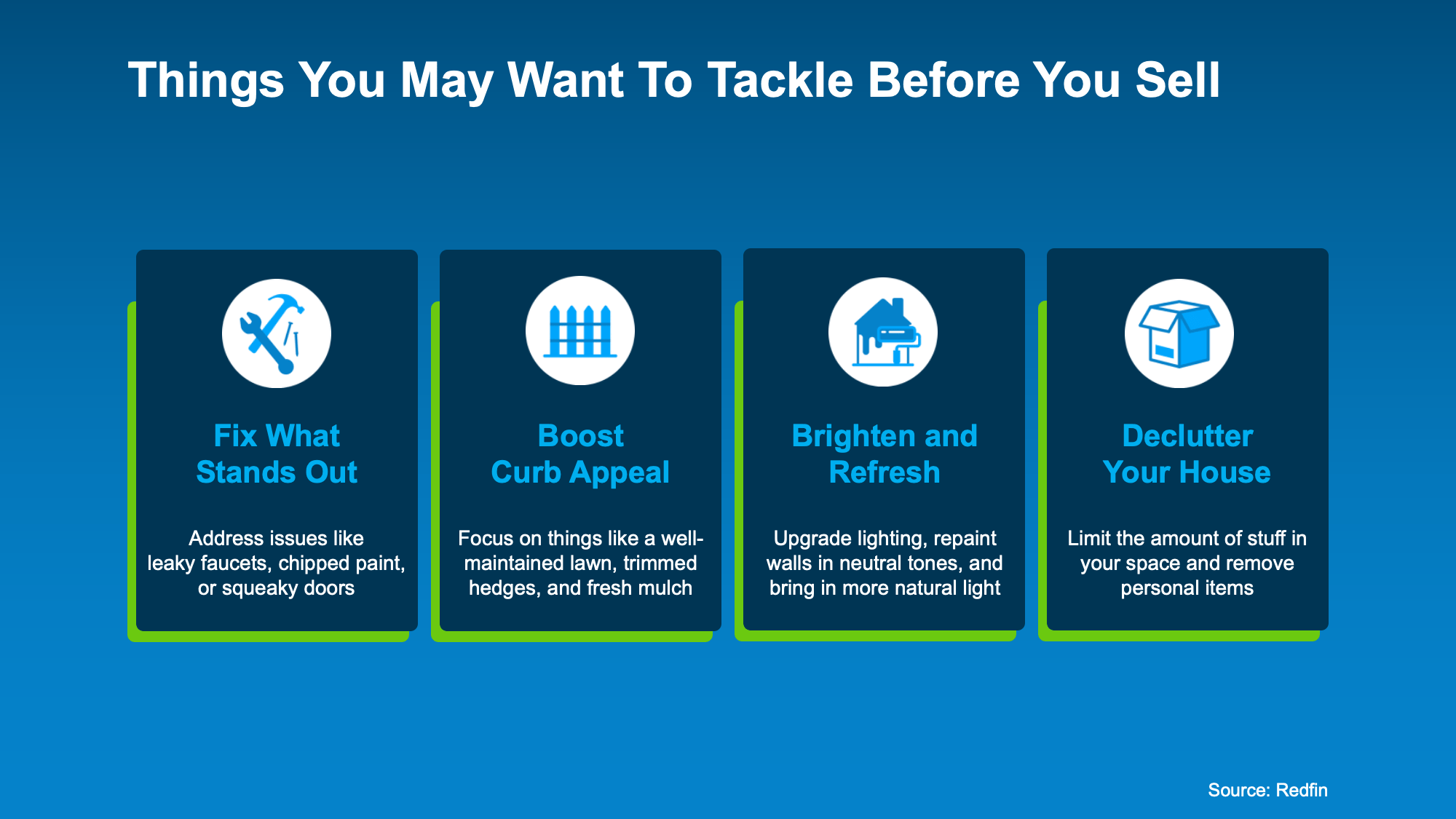

Here's a quick example of things an agent may recommend based on information from Redfin:

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

Bottom Line

Zillow says the best time to list your house is just around the corner. Are you ready to make the most of it?

If you want to take advantage of this Spring sweet spot and get top dollar for your house, let’s talk about what you need to do now to get ready to hit the market.

Monday, April 20, 2026

NAR Existing-Home Sales Report Shows 3.6% Decrease in March

NAR Existing-Home Sales Report Shows 3.6% Decrease in March: Existing-home sales decreased by 3.6% in March 2026. Month over month sales fell in all regions. Year over year sales rose in the South and West and declined in the Northeast and Midwest. Limited inventory continues to drive home prices up.

Friday, April 3, 2026

Before You Fall in Love with a House, Do This First.

Before You Fall in Love with a House, Do This First.

Be honest. Have you started looking at homes online yet? If you have, it’s already time to get pre-approved. Because here’s what not enough people know.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – you don’t want to wait until later on in the process to tackle this step.

No matter what you’ve heard, pre-approval isn’t about commitment. It’s about clarity.

And here are the two big ways pre-approval sets you up for success.

You Know Your Numbers Up Front

During the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. And once you have that number, your search becomes a lot more focused.

With a mortgage pre-approval, you know what you can borrow, so it’s easier to figure out your ideal price point, and what you can actually afford. And that clarity is key.

Because if you just start browsing online and just guess at your price point, you run the risk of falling for a house that’s outside of your price range – or missing out on ones that aren’t.

You want this number to be clearly defined before your search. Here’s why.

You Can Move Quickly When You Find the One

This is how a lot of home searches go today. You scroll through listings just to see what’s out there, and then it happens. You fall in love with something you’ve seen online.

If you’re already pre-approved? You’re probably in great shape.

But if you’re not…

Instead of being able to jump on that house and quickly make an offer, you have to scramble to get a lender, gather the financial documents, and then submit the necessary pre-approval paperwork first. And while you’re waiting to hear back from your lender, someone else who’s more prepared could beat you to the house. As Bankrate explains:

“The best time to get a mortgage preapproval is before you start looking for a home. If you find a home you love but don’t have a preapproval in hand, you likely won’t have time to get preapproved before you need to make an offer . . .”

And that’s avoidable, with the right prep.

Because while you can’t control when the right home shows up, you can be ready for it. Think of it like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

It’s not about rushing your timeline. It’s about removing the delay between finding the right home and being able to move on it.

One Thing You Need To Know About Pre-Approvals

Speaking of timing, pre-approvals do have an expiration date. So, be sure to ask your lender how long it’s good for. The Mortgage Reports explains:

“Mortgage preapproval letters are typically valid for anywhere from 30 to 90 days. However, a preapproval can be updated and extended if the lender re-checks your information.”

Doing the right prep and knowing this information can make the whole process a lot smoother.

You don’t have to be ready to buy to be ready to buy.

Getting pre-approved doesn’t mean you’re committing to buy right now. It just means you’ve taken a step to understand your numbers. And when a home catches your attention, you’re prepped and good to go.

Bottom Line

Ask yourself this: if your perfect home popped up tomorrow, would you be ready to make a move?

If the answer is no and you want to buy, it may be time to get pre-approved. You don’t feel behind before your search even officially kicks off.

Thursday, March 26, 2026

Should You Wait for Lower Rates?

Should You Wait for Lower Rates?

Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they ticked back up into the low 6% range. If you saw that and thought, “Great. I missed it,” you’re not the only one.

A lot of buyers are treating the 5s like some kind of magic number. As if moving from 6.1% to 5.99% suddenly changes everything. And from a mindset perspective, it does feel different.

But here’s the part most people don’t actually run the math on.

The Payment Difference Isn’t What You Think

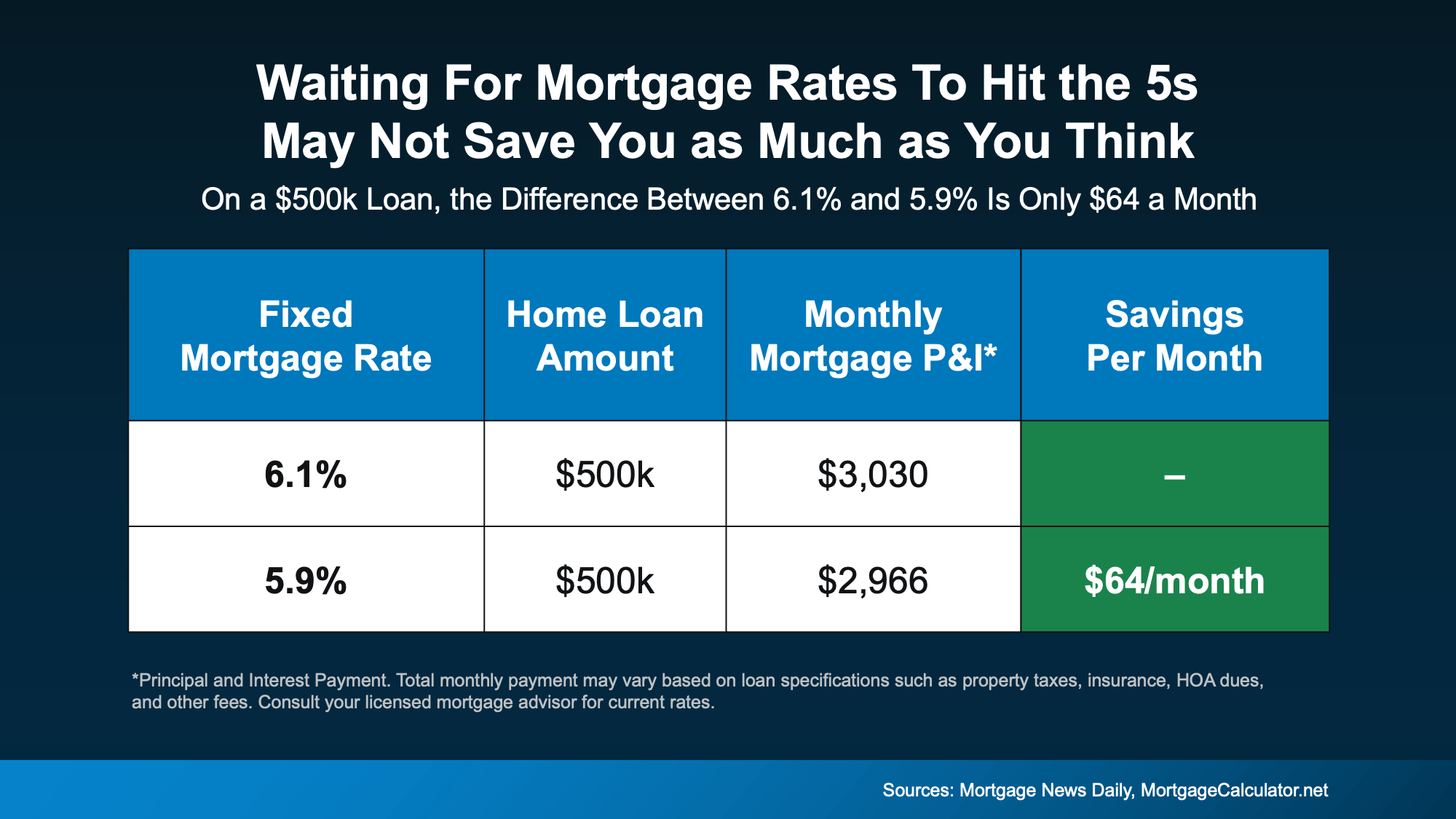

Let’s say you’re looking at a $500,000 home loan. At 6.1%, generally speaking, your principal and interest payment is roughly $3,030 per month. At 5.9%, it’s about $2,966 per month.

That’s a difference of only $64 a month.

Not $300.

Not $500.

Sixty dollars.

Let that sink in for just a moment.

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

The psychological impact of seeing a 5 in front of your rate can feel big. The financial impact? It might be something you don’t even notice when it’s all said and done.

Experts Aren’t Predicting a Big Drop

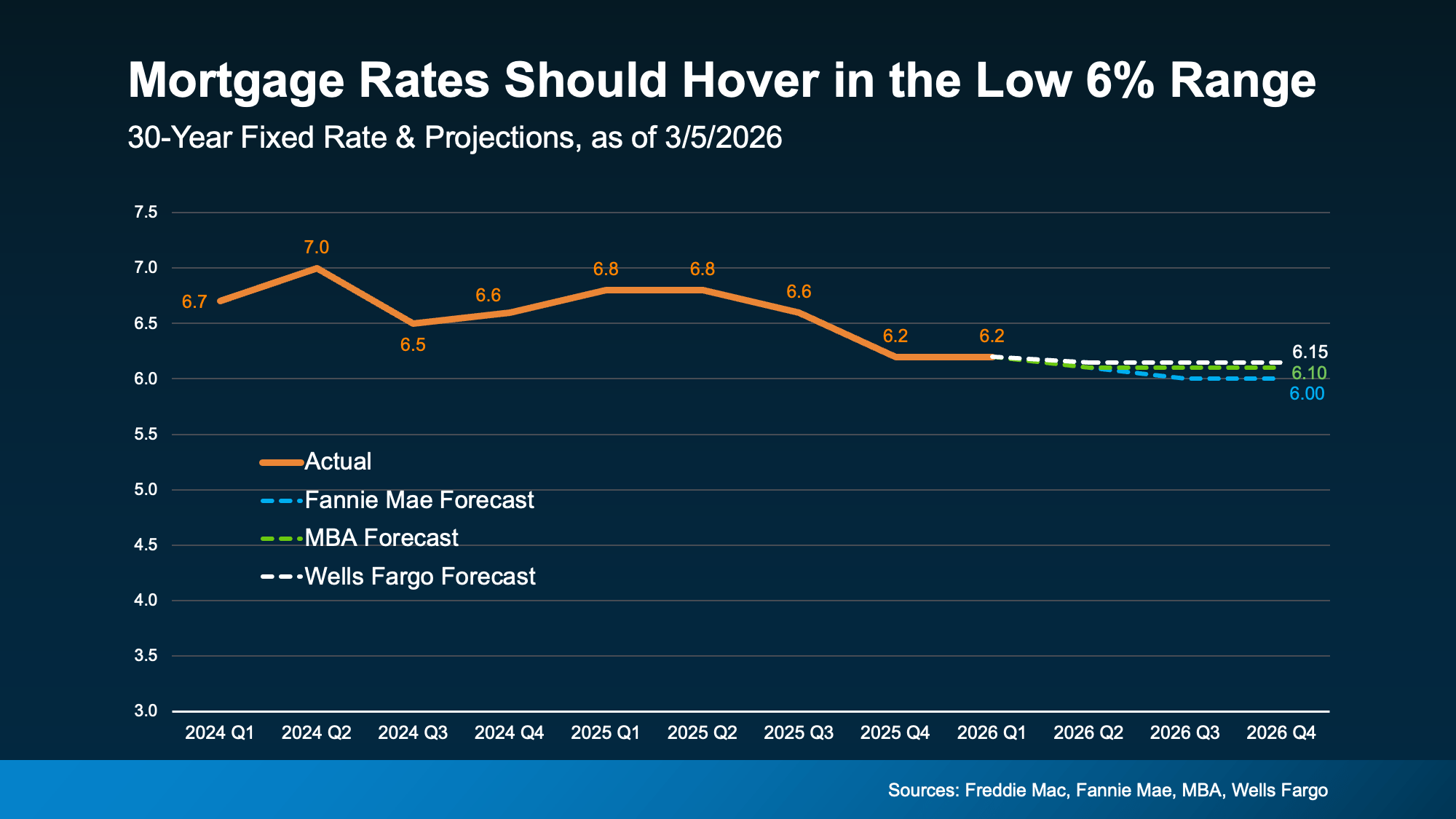

Another important piece to think about: most housing economists aren’t forecasting a long-term return to 5% territory anytime soon.

While rates will move up and down, likely hitting the high 5s here and there, the broader expectation is for mortgage rates to hover in the low 6% range this year, not stay in the 5’s or decline much more.

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

The Bigger Question to Ask

Instead of asking, “Did I miss the 5s?” A better question is: “Does today’s payment work for me?”

If the monthly payment fits comfortably in your budget, and you’ve found a home that meets your needs, the difference between 6.1% and 5.9% likely isn’t the deciding factor. It might be one of them, but it shouldn’t be everything.

And remember, mortgage rates aren’t permanent. If they drop meaningfully later, refinancing is always an option. But you can’t refinance a home you didn’t buy.

Waiting Might Feel Safe, But It Isn’t Always Strategic

It’s natural to want the best possible rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will change things in today’s market.

Don’t miss the fact that rates have already come down. A year ago, they were in the 7s. Now? They’re hovering in the low 6s. And for a lot of people, that percentage point difference that’s already here is the real game changer.

If you paused your plans when rates were higher, now may be the right time to re-run your numbers. Not because rates are “perfect.” But because the monthly payment math might work better than you think, even with rates in the low 6s.

Before assuming you’ve missed your moment, take another look at the numbers.

You may find it never disappeared.

Bottom Line

If you’ve been sitting on the sidelines waiting for that magic number for rates, that strategy may not pay off as much as you’d expect.

Let's connect so you can double check the math at your price point. You may realize payments are already within your range.

Subscribe to:

Posts (Atom)

-

Pending Home Sales Jumped 6.1% in March : The solid rise in pending home sales implies a sizable build-up of potential home buyers, fueled b...

-

Pending Home Sales Waned 4.6% in January : The Midwest, South, and West saw month-over-month losses in transactions, while the Northeast saw...