Monday, August 3, 2026

Foreign Buyers Purchased $45.3 Billion Worth of U.S. Homes from April ‘25 to March ‘26

Foreign Buyers Purchased $45.3 Billion Worth of U.S. Homes from April ‘25 to March ‘26: Foreign buyers purchased 67,100 U.S. homes worth $45.3 billion from April 2025 to March 2026, according to NAR's latest report. Purchases fell 14% and dollar volume declined 19.1% from the prior year. Canada led in buyer share, while China generated the highest dollar volume. Florida remained the top destination for international buyers.

Thursday, July 30, 2026

Buying a Home? Here's What You Should Know About Home Insurance Costs.

Buying a Home? Here's What You Should Know About Home Insurance Costs.

If buying a home is on your radar, you've probably been keeping an eye on mortgage rates and home prices. But don’t forget about homeowners insurance.

Homeowners insurance has always been part of owning a home. But over the past few years, it's become a larger expense for many homeowners – something that's especially frustrating when affordability already feels tight.

The good news? While premiums are still rising, the latest data shows those increases are beginning to slow. Here's what buyers should know.

Home Insurance Costs Have Gone Up

You've probably heard stories from friends or family about their premiums going up. And that’s not really a surprise when you consider data from the Pew Research Center shows 71% of homeowners say their insurance costs have gone up over the past few years.

While no one likes rising costs, knowing what to expect can help you plan ahead. Your first insurance payment is typically included in your closing costs, but after that it'll become part of your monthly housing expenses.

Getting an insurance quote early can help you build a more realistic budget and avoid surprises later.

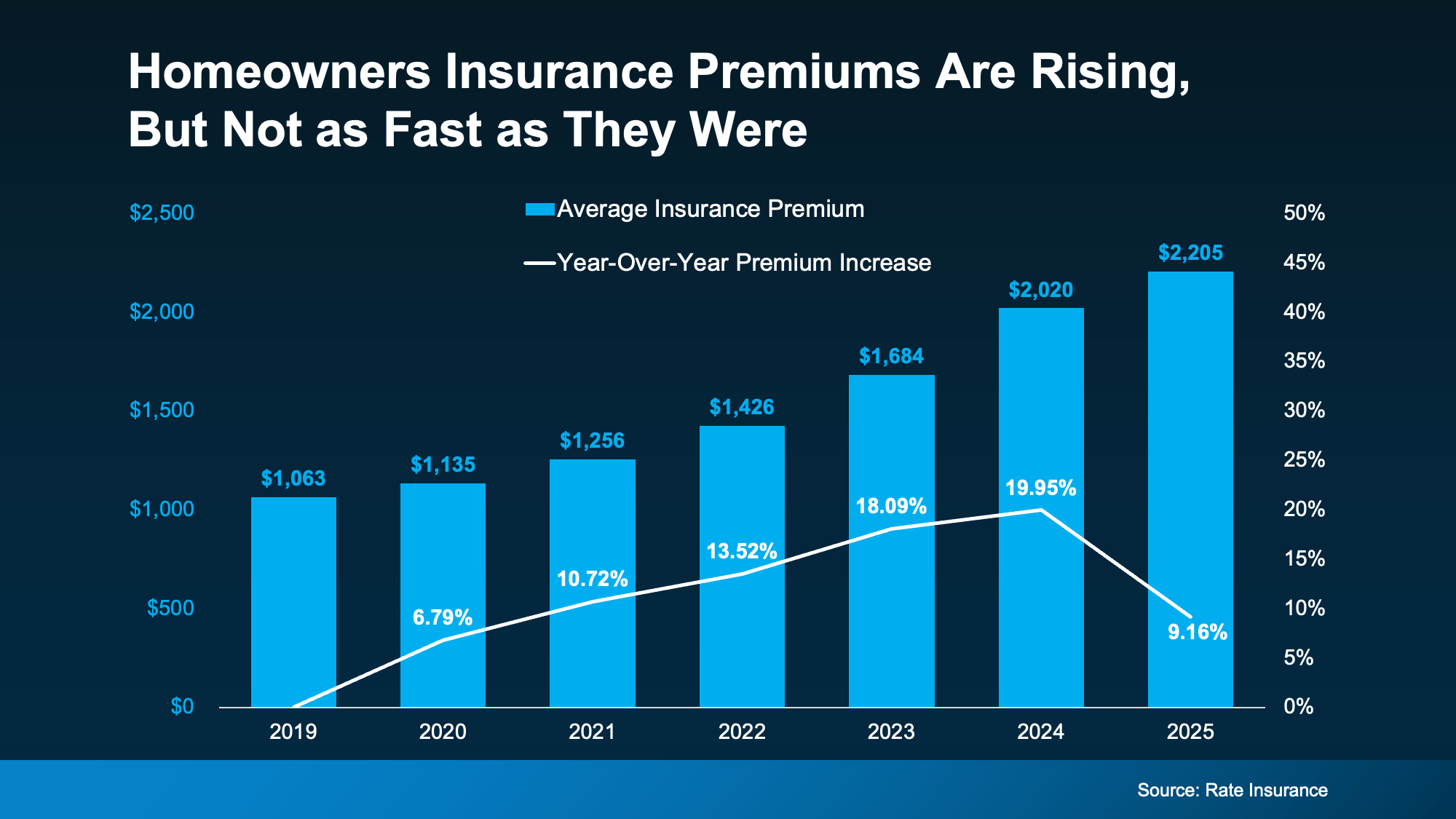

Premiums Are Rising, But Not as Fast as They Were

Most of the headlines focus on how home insurance is getting more expensive. And that's true. But here’s the part that’s easy to miss.

Insurance premiums are still rising.

But they're not rising as fast as they were.

According to the latest report from Rate Insurance, 2025 saw the first slowdown in annual premium increases since 2019 (see graph below):

That doesn't mean premiums are getting cheaper. It simply means the rapid increases of the past several years may finally be starting to ease – a small but welcome step in the right direction.

But what you’ll pay in one part of the country can look very different from what someone pays somewhere else.

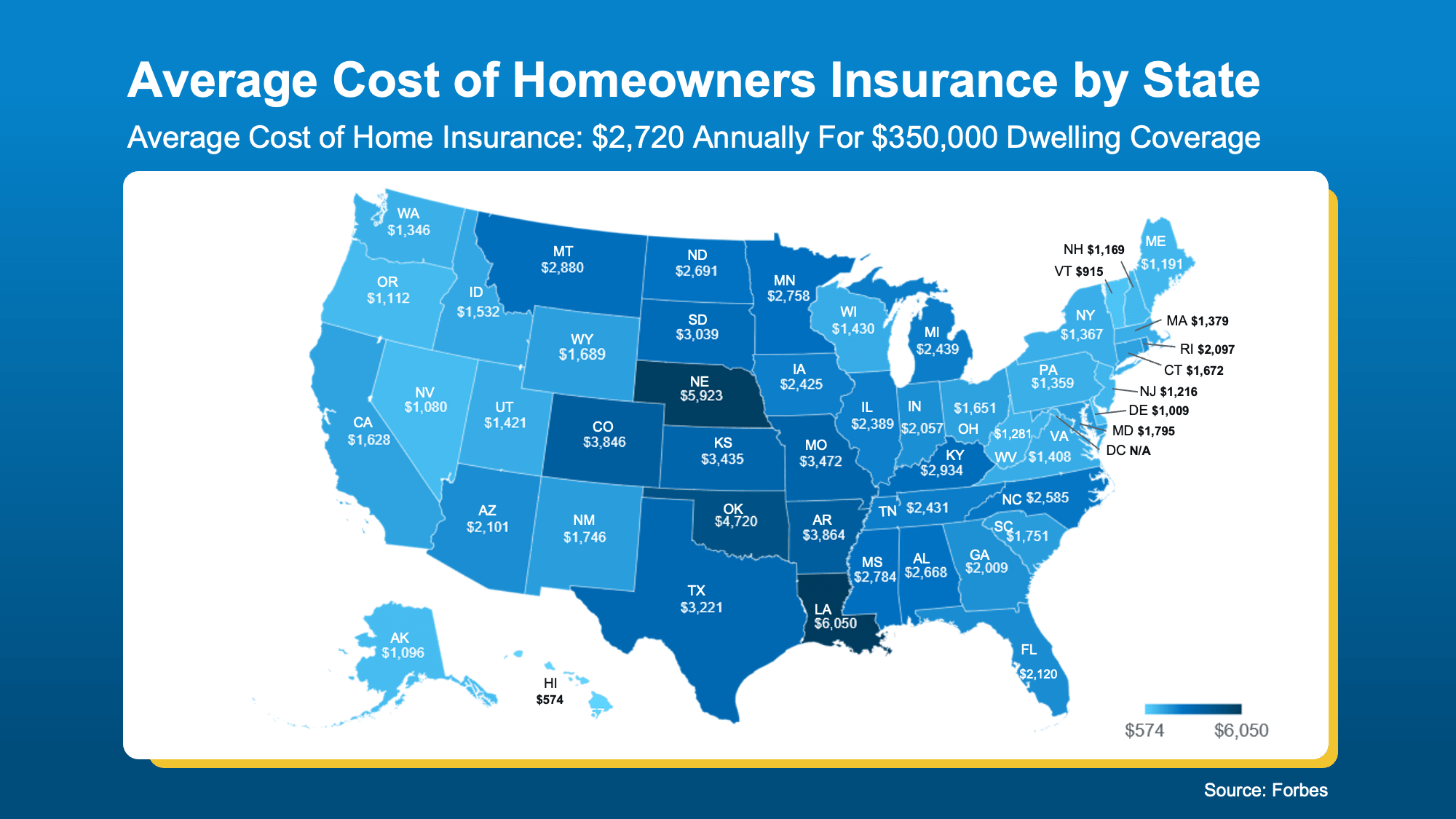

Where You Buy Can Make a Big Difference

Insurance costs vary because some parts of the country experience more claims than others. That's why it's important to look at what's happening locally.

Your premium will depend on things like where you're buying, the home itself, and the coverage you choose.

Forbes data can give a rough idea of your state’s typical premiums. Check out the map below – the darker the blue, the higher the costs tend to be in that state:

Ways To Lower Your Costs

While you can't control every cost that comes with buying a home, you can control how prepared you are. If you’re crunching the numbers and trying to find ways to save, Insurify and NerdWallet offer these tips that can help you get the best insurance price possible:

Shop Around – Compare quotes from multiple companies.

Bundle Policies – Combine home and auto to see if a bundle price is cheaper.

Ask If There Are Discounts – Don’t miss out on savings you may qualify for.

Highlight Upgrades – Features like a new roof or storm windows can cut costs.

Improve Your Credit – A stronger credit score can mean better premiums.

One of the smartest things you can do is get an insurance quote before you make an offer. That way, you'll know what your monthly housing costs are likely to be before you commit.

An insurance professional can walk you through your options and help you find coverage that fits both your needs and your budget.

Bottom Line

Homeowners insurance has become a bigger part of the homebuying conversation. But it doesn't have to become a bigger source of stress.

The key is knowing what to expect before you buy. Get an insurance quote early, factor it into your budget, and lean on trusted local professionals to help you make the most informed decision possible.

Tuesday, July 28, 2026

The “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

The “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

Negotiations are back. More buyers are asking for better deals, and more sellers are giving them. Builders are throwing in extras, too.

That’s why whether you’re buying or selling today, there are two terms you’ll hear a lot: concession and incentive.

A concession is something a seller agrees to during negotiations to get a deal done.

An incentive is a perk a builder (or a seller) advertises upfront to attract buyers.

Let’s run through what you need to know about both and how they could play a role in your move.

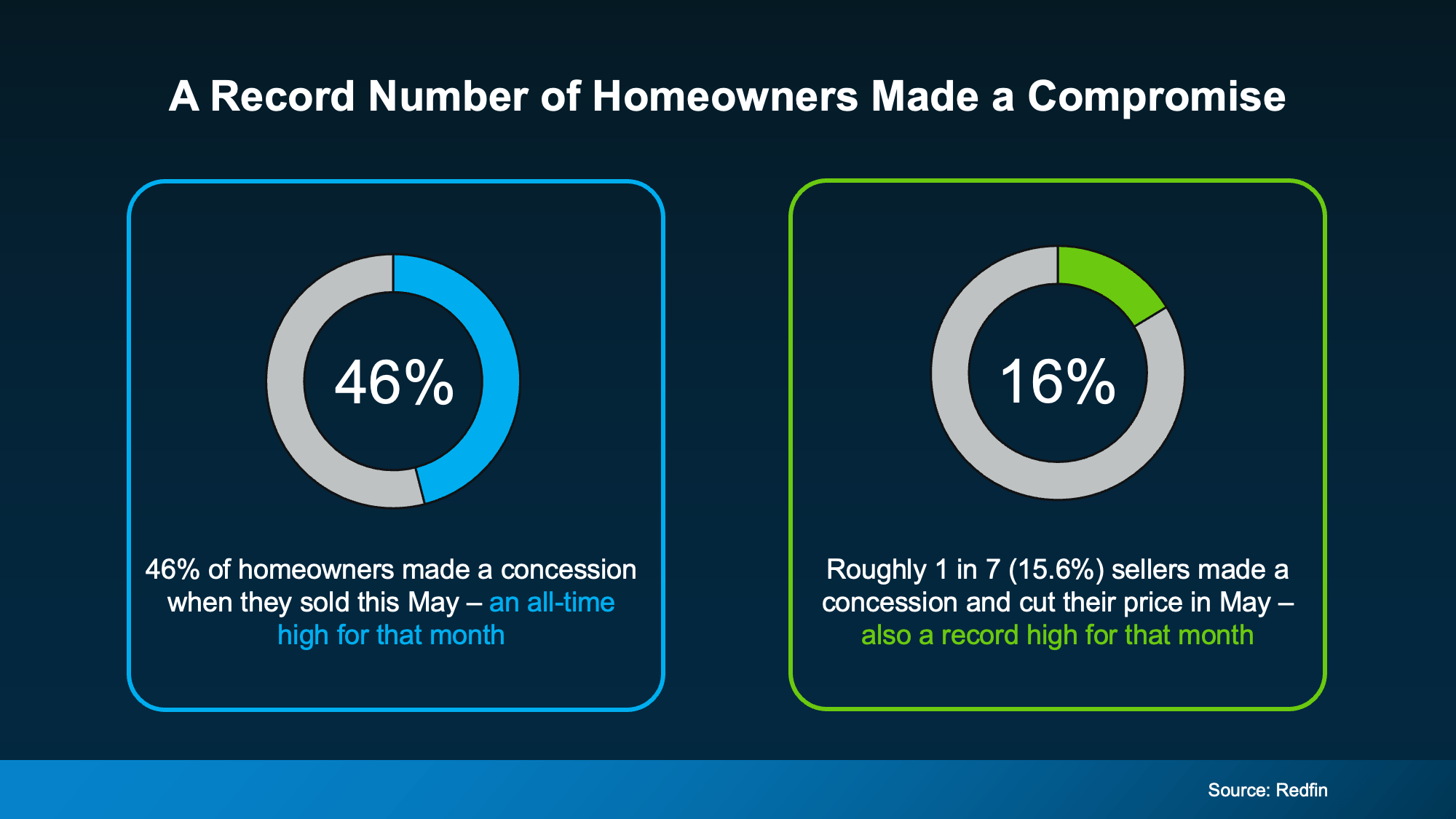

More Sellers Are Agreeing to Concessions

Almost half (46%) of homeowners who sold recently gave the buyer a concession, according to Redfin. That’s the highest share on record for this time of year. And roughly 1 in 7 (16%) sellers went a step further, cutting their asking price and offering a concession on top (see chart below):

So, what kind of concessions are we talking about?

A seller might cover part of your closing costs, take care of a repair, or offer a credit that trims your upfront costs. It’s how they keep a deal on track when buyers have more options to choose from – and homeowners aren’t the only ones compromising.

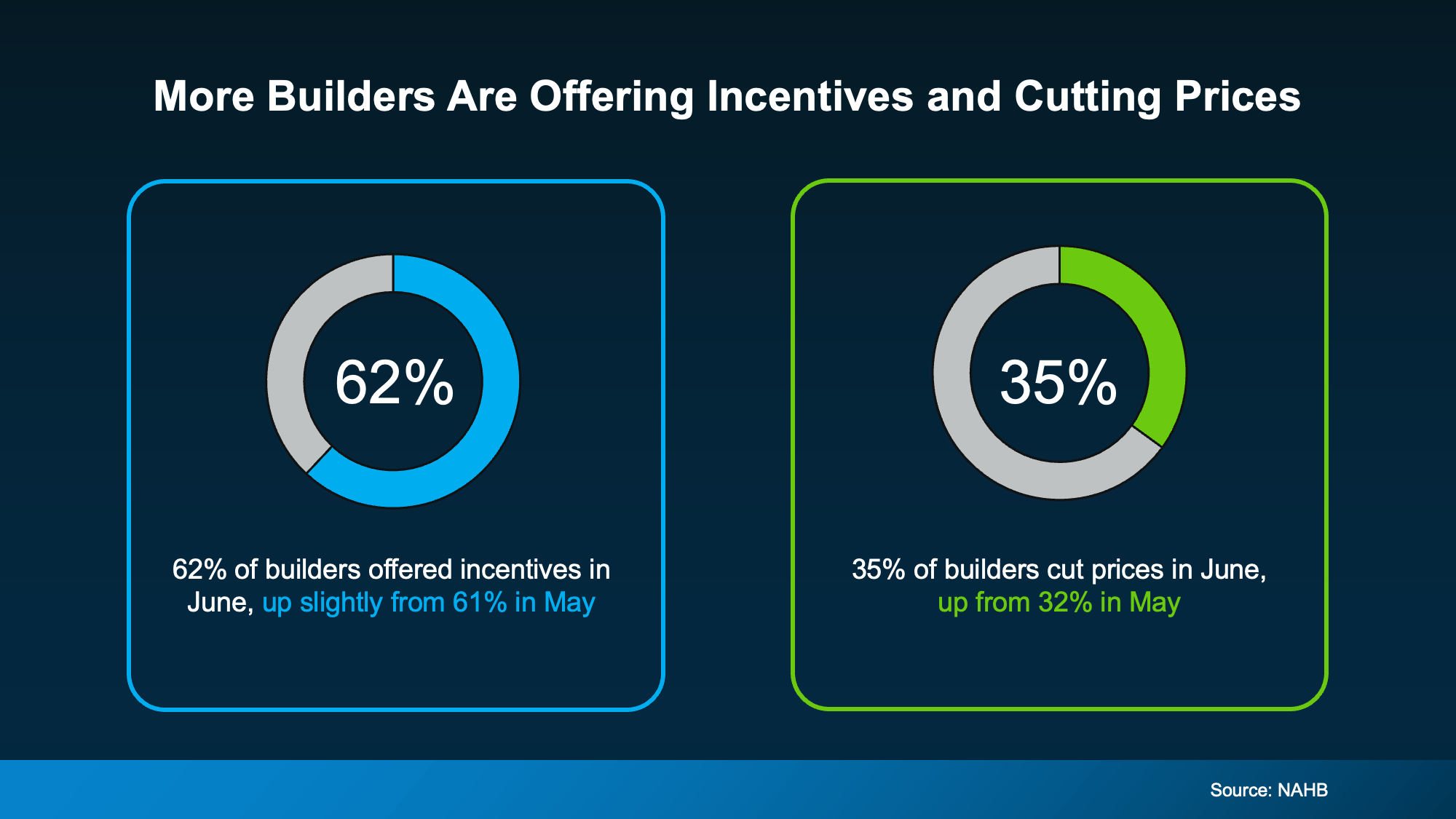

Builders Are Cutting Prices, Too

Newly built homes are seeing the same push and pull. According to the National Association of Home Builders (NAHB), 62% of builders are offering incentives right now. And about 35% are cutting prices outright (see chart below):

Those incentives often look like:

Mortgage rate buydowns

Free upgrades, like nicer finishes or appliances

Danielle Hale, Chief Economist at Realtor.com, explains why:

"New construction has been one of the steadiest parts of the housing market over the past few years, but builders are clearly responding to today's affordability pressures and higher levels of existing-home inventory."

Even builders, who many people think rarely negotiate, are competing on price and perks. They have been for over a year now. The same data shows this is the 15th straight month where more than 60% of builders have offered incentives to sweeten the deal. And that’s significant.

What This Means for Your Move

If you're buying, this is a good time to ask. Whether you have your eye on an existing house or a newly built home, there's a chance the seller or builder will meet you partway on price, terms, or both.

If you're selling, expect buyers to ask. Even builders of brand-new homes are making concessions more often than not right now. Holding firm on every term could mean more time on the market, or a lost sale altogether.

Bottom Line

Sellers and builders are both giving buyers more to work with this year. Want to know what’s realistic to expect in concessions and incentives in our market? Let’s connect.

The House That Started It All Could Kickstart What's Next

The House That Started It All Could Kickstart What's Next

Remember how exciting it was to buy your first place? It felt like crossing a long-awaited finish line. It gave you a place to build your life. Maybe it’s where you lived when you got married. Or where you welcomed a child or a pet into the family.

But that was just the beginning.

For most people, your first house was never meant to be your forever home. It’s a stepping stone for what comes next.

And if your life looks different today than it did when you got the keys, you’re not stuck. Moving may be more realistic than you think.

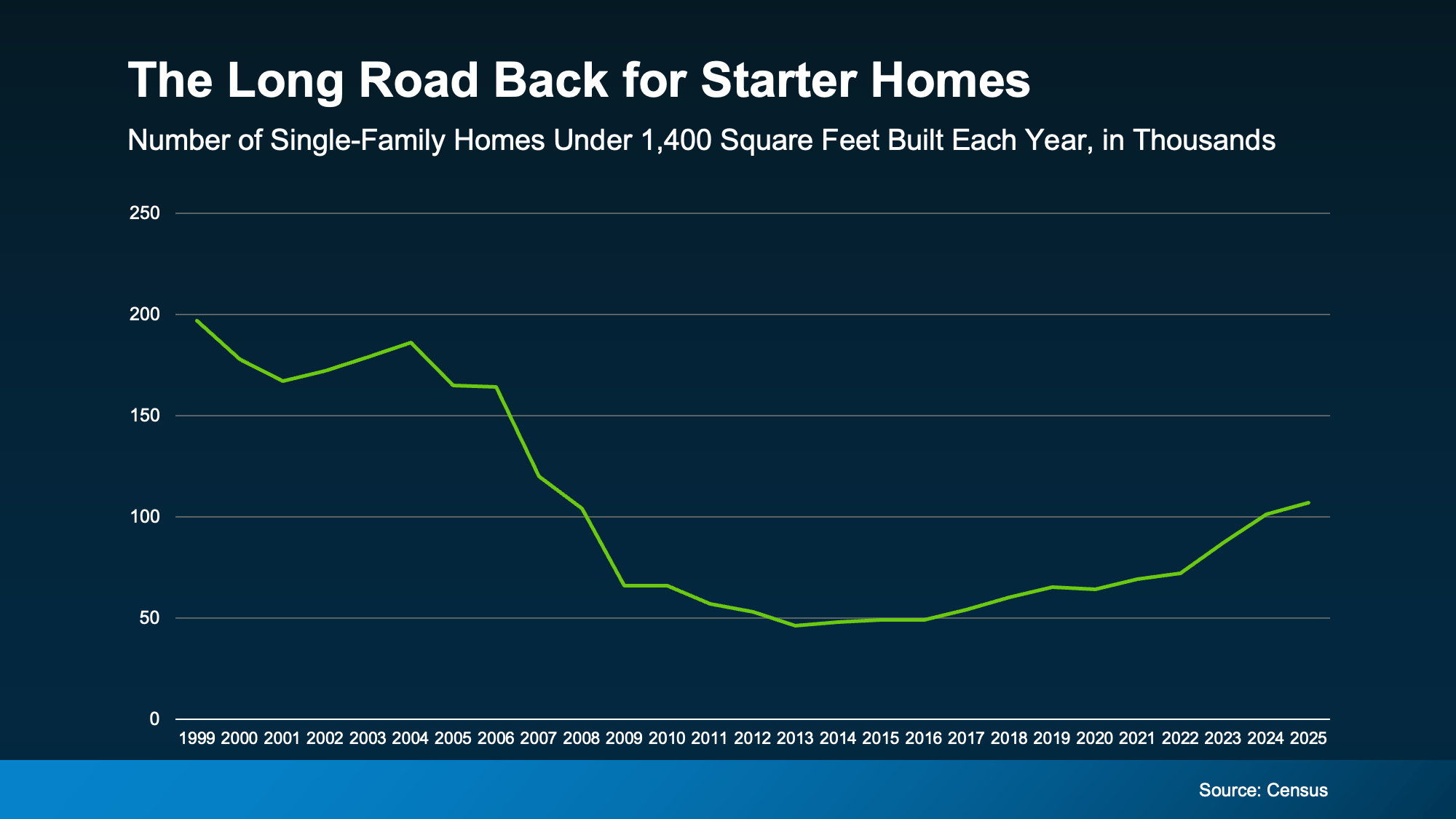

Starter Home Inventory Is Still Relatively Low

If you've been wondering whether now is the right time to move up, here's something worth knowing. Starter homes remain one of the hardest types of homes to find. And that's good news if you're thinking about selling your first place.

Historically, we haven’t been building enough homes for first-time buyers. And even though homebuilders have shifted more attention toward smaller, entry-level homes lately, the Census shows there’s a long way to go to re-build supply (see graph below):

That means your current house is in demand – and that’s a dream scenario for sellers. But that’s only half the story. You also need somewhere to go.

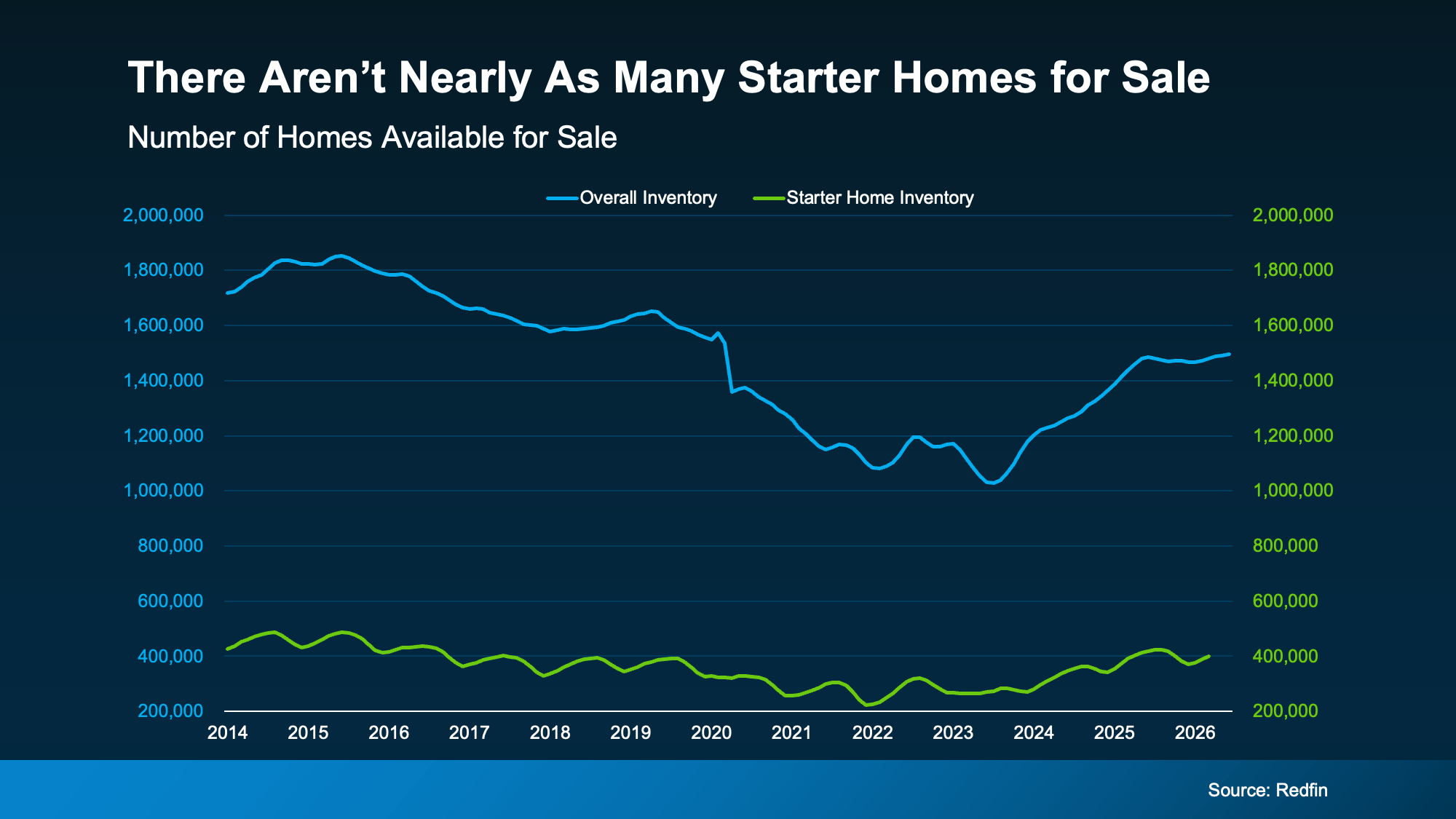

There Are More Move-Up Homes on the Market

Here’s where this gets interesting. While the supply of starter homes remains tight (the green line), data from Redfin shows that the number of homes for sale has been climbing overall (the blue line):

As Nadia Evangelou, Principal Economist and Director of Real Estate Research at the National Association of Realtors (NAR), explains:

“Too much of the inventory available today remains concentrated at higher price points, leaving a shortage of options for entry-level and middle-income buyers.”

That means you may have more choices for your move up than you'd expect. Whether you're hoping for another bedroom, a home office, a bigger backyard, or simply more room for this next stage of life, today's market may finally be giving you the chance to find it.

At the same time, your current house may be exactly what someone else has been looking for because homes like yours are still in short supply. That's a unique advantage for move-up buyers. And it could help you sell for a stronger price. As Zillow says:

"Starter home value appreciation has outpaced other types of homes nationally, mostly because they're so in demand."

Your Biggest Advantage May Be Your Equity

Here’s the cherry on top. There's one more thing your first home has been doing behind the scenes, and that’s building equity. Every mortgage payment you've made and every year your home's value has grown has quietly increased your ownership stake in your house.

According to Cotality, the average homeowner with a mortgage has $295k in equity built up. While your number may be different, once you sell, it could become the down payment on your next home or help reduce the amount you need to borrow at today’s rates.

Put it all together and your move up becomes a lot more realistic than you think:

The house you're selling is in demand.

The house you're buying may be easier to find.

And the equity you've built can help bridge the gap between the two.

Your first home did exactly what it was supposed to do. It gave you a place to start.

Now, it may be the thing that helps you take the next step.

Bottom Line

Your first home was never meant to be your forever home. It was meant to help you build a life and build the financial foundation for whatever came next.

If your current home no longer fits the life you're living today, let’s connect. You may be closer to your next chapter than you realize.

More Homes, Better Prices: A Buyer’s Summer

More Homes, Better Prices: A Buyer’s Summer

If you’ve thought about buying a home in the past few years, you may have run into two frustrations: asking prices that kept climbing and too few homes to choose from.

In many places, both sticking points are letting up this summer, with lower asking prices and more homes for sale. Let’s look at the trends, and what they mean for your search.

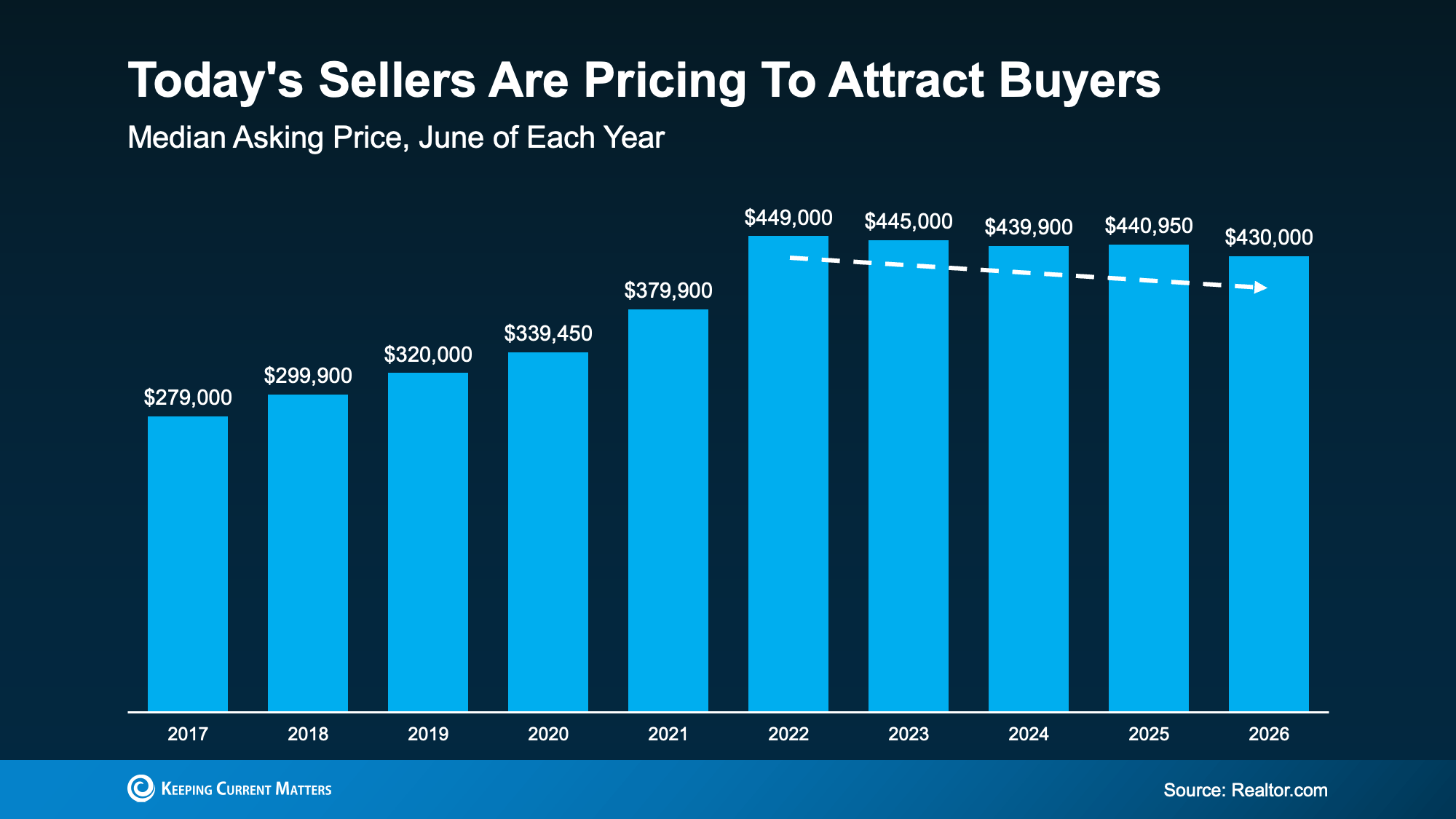

Sellers Are Pricing To Attract Buyers

According to Realtor.com, the national median asking price was $430,000 in June, nearly $11,000 under what it was the year before (see graph below):

That’s the eighth month in a row that the typical asking price has dipped below where they were the previous year, according to the same Realtor.com report.

And while falling prices can sound worrying, this isn’t a sign of an impending crash. We’re talking about asking prices, not sold prices. This is a sign that today’s sellers are meeting the market where it is and pricing to draw buyers. And that’s actually something normal we’d expect from the market. As Danielle Hale, Chief Economist at Realtor.com, puts it:

“Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids. This is a welcome sign that we are in a functioning market.”

Asking prices were never going to climb forever – now they're just settling closer to what buyers can actually pay. That signals a healthier market, and sellers re-adjusting their expectations.

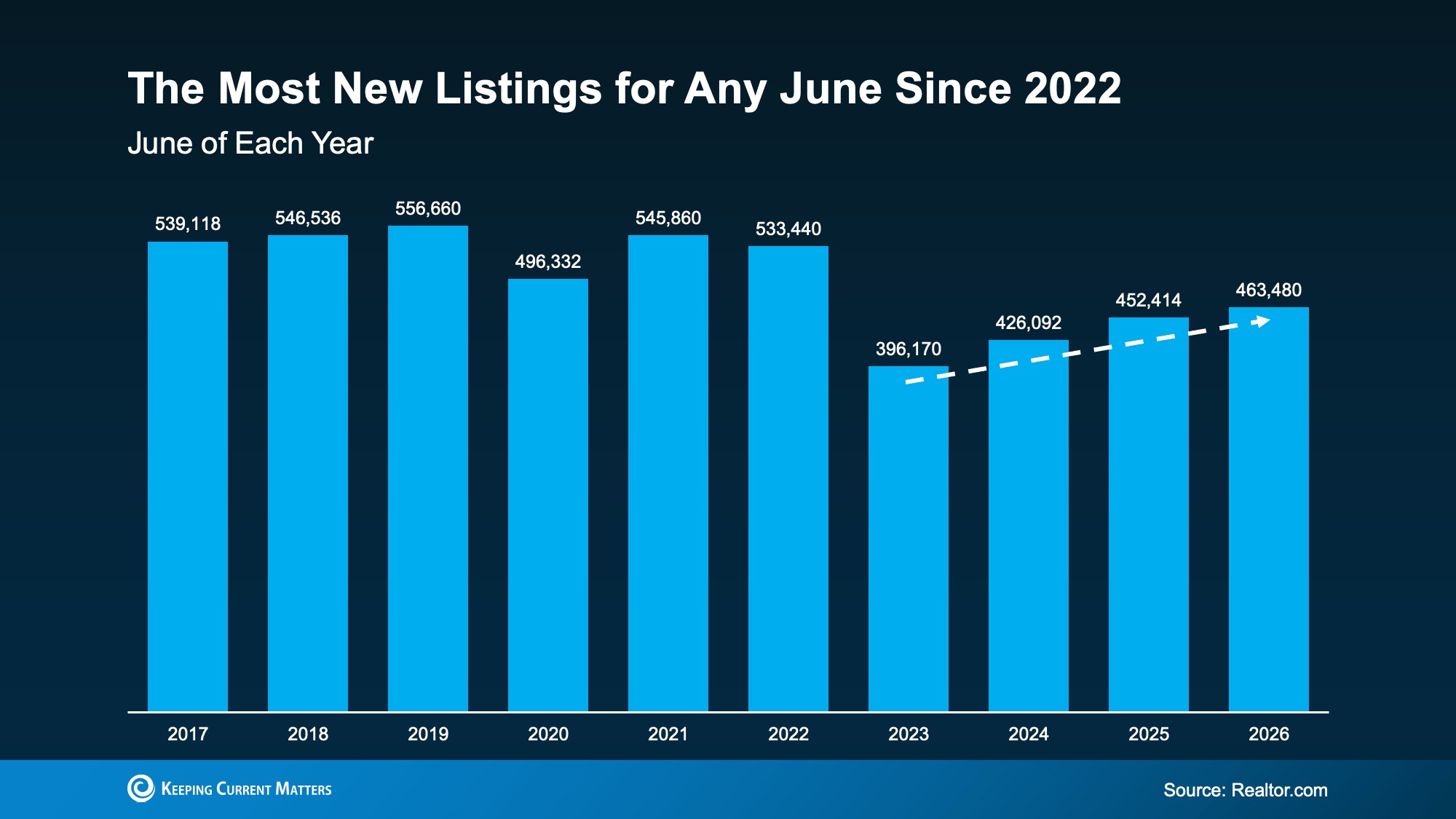

More Homes Are Available Now

If you’ve spent the past few years watching homes disappear before you could even schedule a tour, this is for you.

Supply is starting to catch up. According to Realtor.com, the number of homes listed for sale in June was the highest June number we’ve seen in three years (see graph below):

This means more options for you and less competition for each one.

Now, supply is not back to normal everywhere. As you can see, we’re still down from where we were back in 2017-2019. But in many places, it’s better than it’s been in a while. Here’s how that helps you.

You don’t have to rush an offer just to stay in the running, and you have better odds of finding and landing the right home, not just the one that’s available. Plus, you’ll have more room to negotiate, so you’re searching from a stronger position than buyers had even a year ago.

Why This Is Encouraging if You’re Buying Your First Home

For first-time buyers looking for lower-priced homes, these trends line up especially well. Mischa Fisher, Chief Economist at Zillow, explains:

“The lowest price tiers are exhibiting some softness in terms of price, they also had the most listing-activity growth, the first time since 2022 that’s been the case.”

So, if you’re searching for your first place or your next house, there's a little more to choose from and a little more give on price.

Bottom Line

If a tight budget or a thin selection has kept you from buying a home, now might be the time to restart your search.

Ready to see what’s available here? Let’s connect.

Thursday, July 23, 2026

NAR Pending Home Sales Report Shows 5.4% Decrease in June

NAR Pending Home Sales Report Shows 5.4% Decrease in June: Pending home sales fell 5.4% in June 2026 and were down 0.3% from a year ago, as elevated mortgage rates and record-high home prices continued to challenge buyers. Contract signings declined across all four U.S. regions month over month, though the Northeast and Midwest posted modest annual gains.

Friday, July 17, 2026

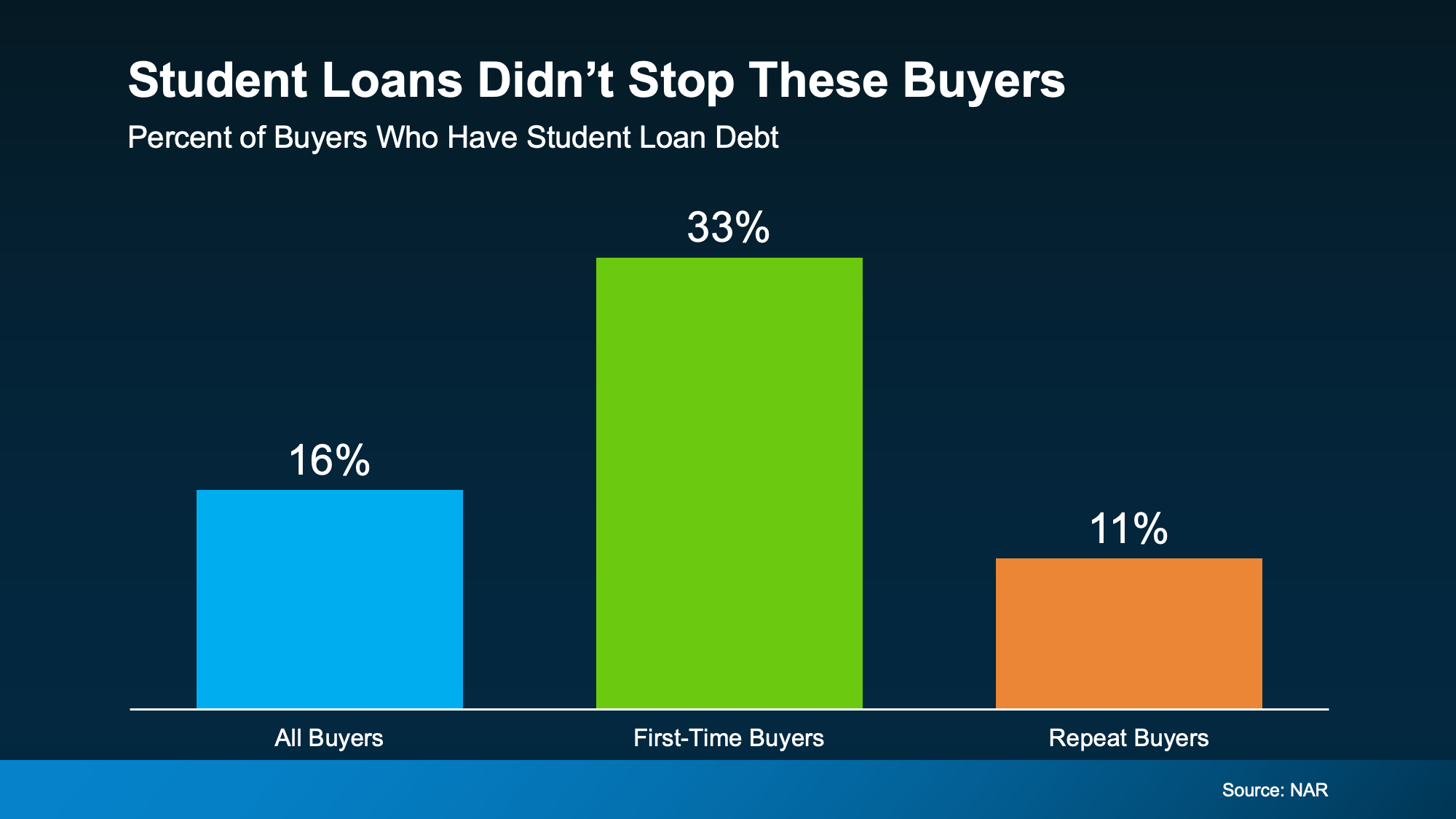

Student Loans Are Back in the News. Don't Let It Put Your Homeownership Plans on Hold.

Student Loans Are Back in the News. Don't Let It Put Your Homeownership Plans on Hold.

Student loans are back in the spotlight. And whether you've been following the headlines closely or just catching bits and pieces here and there, there's a good chance they've been on your mind lately.

And if you’re questioning whether you have to hit pause on your plans to buy a home, here's the thing you have to remember:

Having student loans doesn't automatically mean buying a home has to wait.

The Biggest Myth About Student Loans and Buying a Home

One of the most common misconceptions among first-time buyers is that they have to pay off their student loans before they can qualify for a mortgage. But in most cases, that's just not true.

As an article from Redfin explains, student loans usually get evaluated the same way other debts do, like credit cards or car payments:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

So having that loan on your credit report isn't some special red flag that immediately disqualifies you.

Instead, lenders look at your overall financial situation, including your income, credit history, and more. Student loans are one piece of that puzzle, but they’re not the entire picture.

You're in Better Company Than You Think

Just to really drive this home, here’s a stat from the National Association of Realtors (NAR) that proves you can have student debt and still buy a home. Their research shows 33% of first-time homebuyers still had student loan debt.

That's 1 out of every 3 first-time buyers. The median amount they owed? $30,400.

Let that reassure you that people are buying homes with student debt every day. And carrying student loans doesn't automatically put homeownership out of reach.

Don’t Count Yourself Out Before You Even Try

At the end of the day, here's where a lot of buyers trip themselves up. They assume the worst and never even check what they could actually qualify for. But your situation is more unique than a blanket "no."

If your income is steady and the rest of your finances are in decent shape, buying a home could be more realistic than you think. The only way to know for sure is to actually run the numbers with someone who does this for a living.

You may discover you're closer to buying than you think.

Bottom Line

Student loans don't have to be the thing standing between you and owning a home. If you've been putting off your homebuying plans because of that debt, talk to a lender about your options. It may not be the barrier you think it is.

Subscribe to:

Posts (Atom)

-

Pending Home Sales Jumped 6.1% in March : The solid rise in pending home sales implies a sizable build-up of potential home buyers, fueled b...

-

Pending Home Sales Waned 4.6% in January : The Midwest, South, and West saw month-over-month losses in transactions, while the Northeast saw...