Tuesday, April 30, 2024

Pending Home Sales Ascended 3.4% in March

Pending Home Sales Ascended 3.4% in March: NAR forecasts 4.46 million existing-home sales in 2024, a 9% increase from 2023.

Monday, April 29, 2024

The Best Way To Keep Track of Mortgage Rate Trends

The Best Way To Keep Track of Mortgage Rate Trends

If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.

The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know.

The Latest on Mortgage Rates

Rates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors.

Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

Professionals Can Help Make Sense of it All

While you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of work. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, lean on the pros.

They coach people through market conditions all the time. They’ll focus on giving you a quick summary of any broader trends up or down, what experts say lies ahead, and how all of that impacts you.

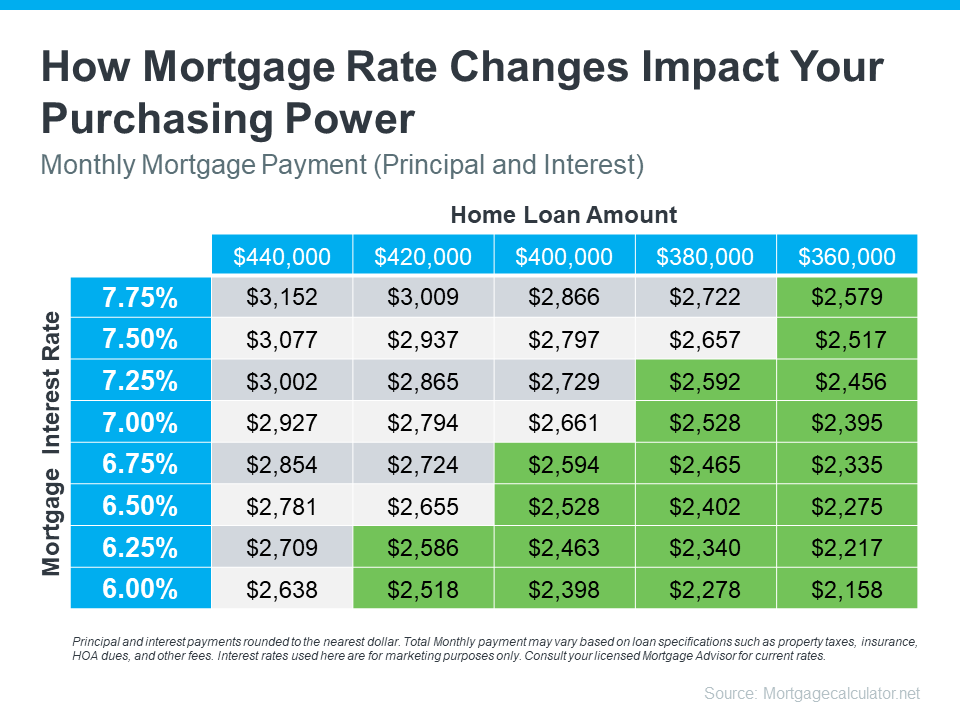

Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

As you can see, even a small shift in rates can impact the loan amount you can afford if you want to stay within that target budget.

It’s tools and visuals like these that take everything that’s happening and show what it actually means for you. And only a pro has the knowledge and expertise needed to guide you through them.

You don’t need to be an expert on real estate or mortgage rates, you just need to have someone who is, by your side.

Bottom Line

Have questions about what’s going on in the housing market? Let’s connect so we can take what’s happening right now and figure out what it really means for you.

Thursday, April 25, 2024

Foreclosure Numbers Are Nothing Like the 2008 Crash

Foreclosure Numbers Are Nothing Like the 2008 Crash

If you’ve been keeping up with the news lately, you’ve probably come across some articles saying the number of foreclosures in today’s housing market is going up. And that may leave you feeling a bit worried about what’s ahead, especially if you owned a home during the housing crash in 2008.

The reality is, while increasing, the data shows a foreclosure crisis is not where the market is headed.

Here’s the latest information stacked against the historical data to put your mind at ease.

The Headlines Make the Increase Sound Dramatic – But It’s Not

The increase the media is calling attention to is a little bit misleading. That’s because it’s comparing the most recent numbers to a time when foreclosures were at historic lows. And that lopsided comparison is making it sound like a much bigger deal than it actually is.

Back in 2020 and 2021, there was a moratorium and forbearance program that helped millions of homeowners avoid foreclosure during challenging times. That’s why numbers for just a few years ago were so low.

Now that the moratorium has come to an end, foreclosures are resuming and that means numbers are rising. But it’s an expected increase, not a surprise, and not a cause for alarm. Just because foreclosure filings are up doesn’t mean the housing market is in trouble.

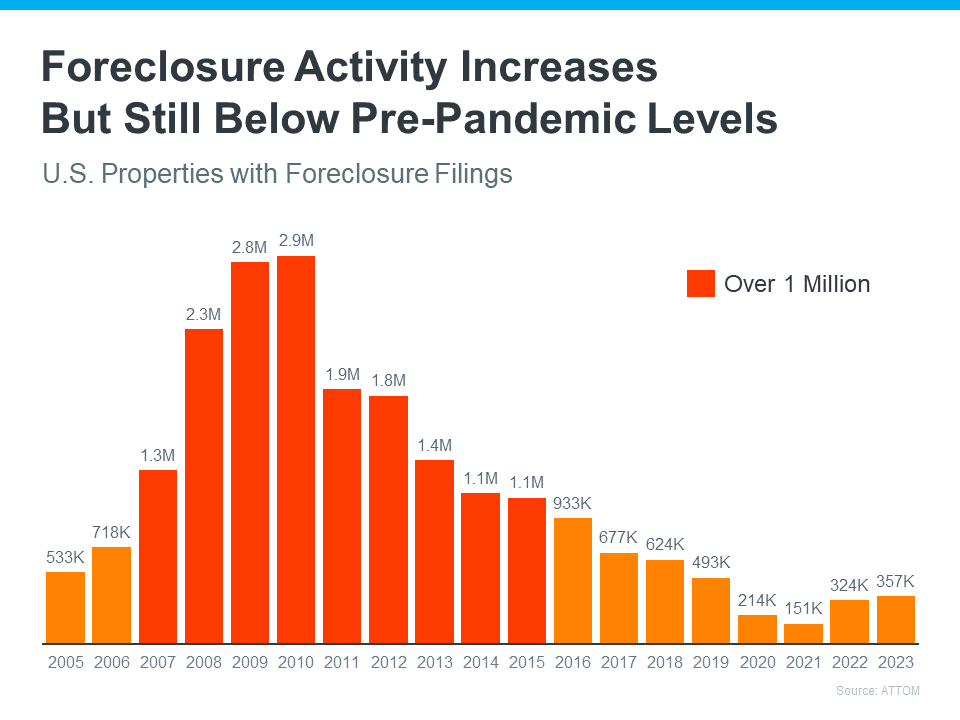

To prove that to you, let’s expand the comparison out a bit more. Specifically, we’ll go all the way back to the housing crash in 2008 – since that’s what people worry may happen again.

The graph below uses research from ATTOM, a property data provider, to show foreclosure activity has been consistently lower since the crash in 2008:

What the data shows is that things now aren’t anything like they were surrounding the housing crash. The bars in red are when there were over 1 million foreclosure filings a year. In 2023, there were roughly 357,000. That’s a big difference.

A recent article from Bankrate explains one of the reasons things aren’t like they were back then:

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.”

Basically, foreclosure activity is nothing like it was during the crash. That’s because most homeowners today have enough equity to keep them from going into foreclosure. And that’s a really good thing for homeowners and for the market.

The reality is, the data shows a foreclosure crisis is not where the market is today, or where it’s headed.

Bottom Line

Right now, putting the data into context is more important than ever. While the housing market is experiencing an expected rise in foreclosures, it’s nowhere near the crisis levels seen when the housing bubble burst, and that won’t lead to a crash in home prices.

Subscribe to:

Comments (Atom)

Should You Wait for Lower Rates?

Should You Wait for Lower Rates? Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they t...

-

Pending Home Sales Jumped 6.1% in March : The solid rise in pending home sales implies a sizable build-up of potential home buyers, fueled b...

-

Pending Home Sales Waned 4.6% in January : The Midwest, South, and West saw month-over-month losses in transactions, while the Northeast saw...