Wednesday, December 7, 2022

Realtors®’ CEO Meets with White House Officials to Discuss Housing Supply, Affordability

Realtors®’ CEO Meets with White House Officials to Discuss Housing Supply, Affordability: NAR continues to stress that government must invest in boosting our nation’s housing supply if we are to make housing affordable in the long run.

Monday, December 5, 2022

Pending Home Sales Declined 4.6% in October

Pending Home Sales Declined 4.6% in October: Month-over-month, contract signings fell in three of four major U.S. regions in October 2022, while the Midwest registered an increase; pending sales declined in all regions compared to one year ago.

Monday, November 21, 2022

Mortgage Rates Will Come Down, It’s Just a Matter of Time

Mortgage Rates Will Come Down, It’s Just a Matter of Time

This past year, rising mortgage rates have slowed the red-hot housing market. Over the past nine months, we’ve seen fewer homes sold than the previous month as home price growth has slowed. All of this is due to the fact that the average 30-year fixed mortgage rate has doubled this year, severely limiting homebuying power for consumers. And, this month, the average rate for financing a home briefly rose over 7% before coming back down into the high 6% range. But we’re starting to see a hint of what mortgage interest rates could look like next year.

Inflation Is the Enemy of Long-Term Interest Rates

As long as inflation is high, we’ll see higher mortgage rates. Over the past couple of weeks, we’ve seen indications that inflation may be cooling, giving us a glimpse into what may happen in the future. The mortgage market is eagerly awaiting positive news on inflation. As Ali Wolf, Chief Economist at Zonda, says:

“The housing market is expected to face continued uncertainty heading into 2023 as consumers, financial markets, and policymakers work through their respective challenges in today’s economy. . . . we are watching for any additional stability in the MBS market, signs of cooling inflation, and/or less aggressive Federal Reserve action to give us confidence that mortgage rates are past their peak.”

What Does This Mean for the Future of Mortgage Rates?

As we get through the inflation battle and start to see that coming down, we should expect mortgage rates to follow. We’ve seen nods of this over the past couple of weeks. As the Federal Reserve works to bring inflation down, mortgage rates will come down as well. Bill McBride from Calculated Risk says:

“My current view is inflation will ease quicker than the Fed currently expects.”

As we look toward next year, we certainly hope he’s right.

Bottom Line

Mortgage rates will come down – it’s just a matter of time. The hope is we continue to see more positive news on inflation, and that’ll bring mortgage rates down. This will give prospective homebuyers more buying power and lead to more homeowners throughout the country.

Thursday, November 17, 2022

VA Loans Can Help Veterans Achieve Their Dream of Homeownership

VA Loans Can Help Veterans Achieve Their Dream of Homeownership

For over 78 years, Veterans Affairs (VA) home loans have provided millions of veterans with the opportunity to purchase homes of their own. If you or a loved one have served, it’s important to understand this program and its benefits.

Here are some things you should know about VA loans before you start the homebuying process.

What Are VA Loans?

VA home loans provide a pathway to homeownership for those who have served our nation. The U.S. Department of Veterans Affairs describes the program like this:

“VA helps Servicemembers, Veterans, and eligible surviving spouses become homeowners. As part of our mission to serve you, we provide a home loan guaranty benefit and other housing-related programs to help you buy, build, repair, retain, or adapt a home for your own personal occupancy.”

Top Benefits of the VA Home Loan Program

In addition to helping eligible buyers achieve their homeownership dreams, VA loans have several other great benefits for buyers who qualify. According to the Department of Veteran Affairs:

- Qualified borrowers can often purchase a home with no down payment.

- Many other loans with down payments under 20% require Private Mortgage Insurance (PMI). VA Loans do not require PMI, which means veterans can save on their monthly housing costs.

- VA-Backed Loans often offer competitive terms and mortgage interest rates.

A recent article from Veterans United sums up just how impactful this loan option can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

John Bell, Acting Executive Director of the Department of Veterans Affairs Loan Guaranty Service, also explains why this program is so powerful:

“It provides early ownership for many people that would not have that opportunity to begin with. Since there’s no down payment, it allows people to hold their wealth and it gives them the ability to have long term financial security by being able to own a house and let that equity grow.”

Bottom Line

Homeownership is the American Dream. Our veterans sacrifice so much in service of our nation, and one way we can honor and thank them is to ensure they have the best information about the benefits of VA home loans. Thank you for your service.

Key Factors Affecting Home Affordability Today

Key Factors Affecting Home Affordability Today

Every time there’s a news segment about the housing market, we hear about the affordability challenges buyers are facing today. Those headlines are focused on how much mortgage rates have climbed this year. And while it’s true rates have risen dramatically, it’s important to remember they aren’t the only factor in the affordability equation.

Here are three measures used to establish home affordability: home prices, mortgage rates, and wages. Let’s look closely at each one.

1. Mortgage Rates

This is the factor most people are focused on when they talk about homebuying conditions today. So far, current rates are almost four full percentage points higher than they were at the beginning of the year. As Len Kiefer, Deputy Chief Economist at Freddie Mac, explains:

“U.S. 30-year fixed mortgage rates have increased 3.83 percentage points since the end of last year. That's the biggest year-to-date increase in rates in over 50 years.”

That increase in mortgage rates is impacting how much it costs to finance a home purchase, creating a challenge for many buyers that’s pricing some out of the market. While the current global uncertainty makes it difficult to project where mortgage rates will go in the future, experts do say that rates will likely remain high as long as inflation does.

2. Home Prices

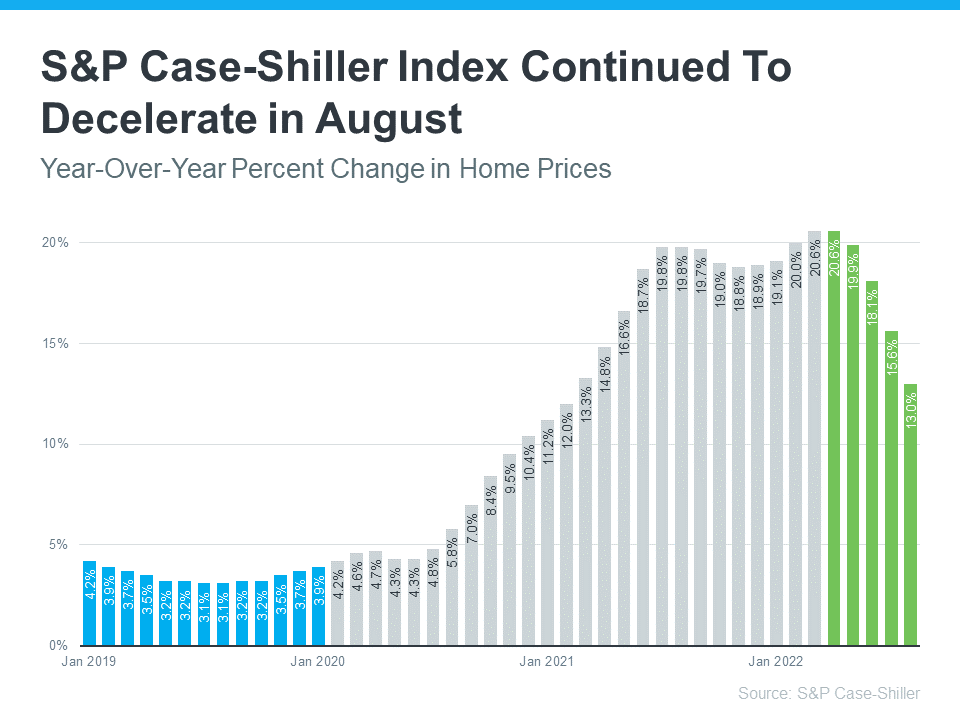

The second factor at play is home prices. Home prices have made headlines over the past few years because they skyrocketed during the pandemic. Now, the most recent Home Price Index from S&P Case-Shiller shows home values continued to decelerate for a fifth consecutive month (shown in green in the graph below):

This deceleration is happening because higher mortgage rates are moderating demand, and as a result, easing the buyer competition and bidding wars that previously drove prices up.

What’s worth noting though, is how much higher home prices still are than they were before the pandemic (shown in blue in the graph above). Even now, we have a long way to go to get to more normal levels of home price appreciation, which is historically closer to 4%. When both mortgage rates and home prices are high, affordability and your purchasing power become a greater challenge.

But while prices are still elevated in many markets, some areas are seeing slight declines. It all depends on your local market. For insight into what’s happening in your area, reach out to a trusted real estate professional.

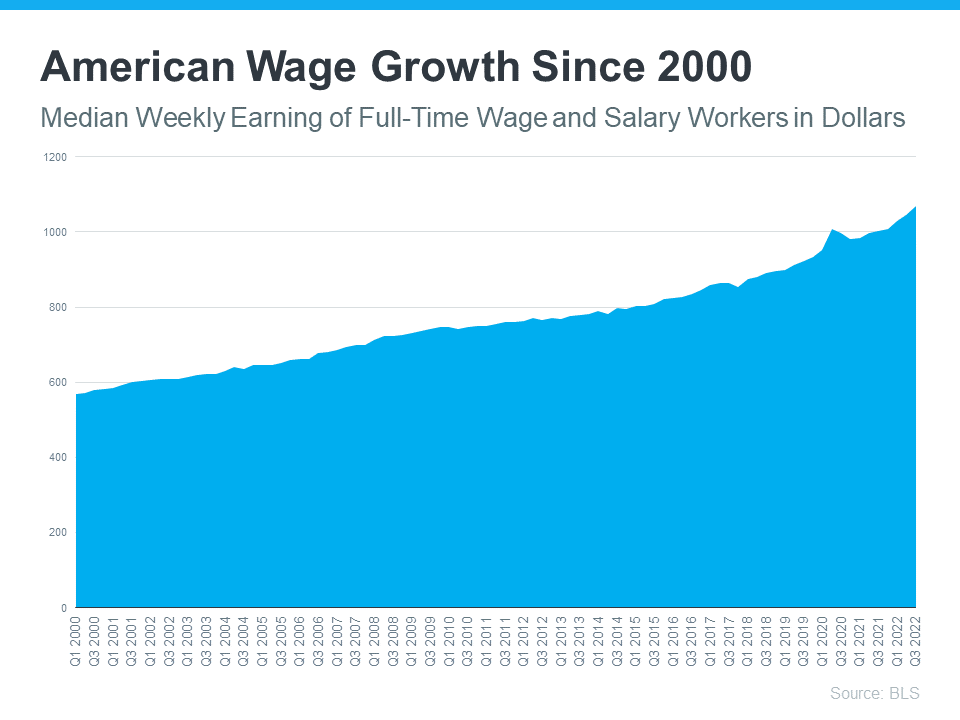

3. Wages

The one big, positive component in the affordability equation is the increase in American wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time. This year is no exception.

As the Bureau of Labor Statistics (BLS) reports:

“Median weekly earnings of the nation's 120.2 million full-time wage and salary workers were $1,070 in the third quarter of 2022 (not seasonally adjusted), the U.S. Bureau of Labor Statistics reported…This was 6.9 percent higher than a year earlier…”

So, when you think about affordability, remember the full picture includes more than just mortgage rates. Home prices and wages need to be factored in as well. Because wages have been rising, they’re a big reason why serious buyers are still purchasing homes this year.

If you have questions or want to learn more, reach out to a trusted advisor who can explain how all of these variables work together and what’s happening in your area. As Leslie Rouda Smith, President of the National Association of Realtors (NAR), says:

“Buying or selling a home involves a series of requirements and variables, and it's important to have someone in your corner from start to finish to make the process as smooth as possible… and objectivity to deliver trusted expertise to consumers in every U.S. ZIP code.”

Bottom Line

To learn more, let’s connect today and make sure you have a trusted lender so you’re able to make an informed decision if you’re planning to buy or sell a home right now.

VA Loans: Making Homes for the Brave Achievable [INFOGRAPHIC]

VA Loans: Making Homes for the Brave Achievable [INFOGRAPHIC]

![VA Loans: Making Homes for the Brave Achievable [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/11/09154718/VA-Loans-Making-Homes-For-The-Brave-Achievable-MEM-1046x2014.png)

Some Highlights

- VA Loans can help make homeownership possible for those who have served our country.

- These loans offer great benefits for eligible individuals and can help them buy a VA-approved house or condo, build a new home, or make improvements to their house.

- Homeownership is the American Dream. One way we can honor and thank our veterans is to ensure they have the best information about the benefits of VA home loans.

More People Are Finding the Benefits of Multigenerational Households Today

More People Are Finding the Benefits of Multigenerational Households Today

If you’re thinking of buying a home and living with siblings, parents, or grandparents, then multigenerational living may be for you. The Pew Research Center defines a multigenerational household as a home with two or more adult generations. And the number of individuals choosing multigenerational living has increased over the past 50 years.

As you consider this option for your own home search, know it could help you on your homeownership journey and provide you with other incredible benefits along the way.

Living with Loved Ones Could Help You Achieve Your Homeownership Goals

There are several reasons people choose to live in a multigenerational household, and for many, the arrangement is a personal one. But according to the Pew Research Center, the top reason people choose to live together today is financial.

A recent study from Freddie Mac also finds more people are choosing to buy a home together so they can save money in the homebuying process. As the study says:

“. . . an increasing percentage of young adult first-time homebuyers are relying on support from older generations, including their parents, to buy a home together.”

For these individuals, combining their resources can help them achieve their dream of buying and owning a home. By pooling their incomes together to make that purchase, they may be able to afford a home they couldn’t on their own.

Other Key Benefits of Multigenerational Living

Not to mention, living in a home with loved ones can have other benefits too, like giving you more quality time to spend together. Darla Mercado, Certified Financial Planner and Markets Editor for CNBC.com, explains how this living arrangement can help on a personal and financial level:

“Residing with relatives can offer advantages . . . you can pool multiple streams of income, for instance. And in households with young children, grandparents can pitch in with child care.”

If this sounds like a great option for you, it’s important to work with a trusted real estate professional to discuss your needs. They can help you navigate the process to find the right home for you and your loved ones.

Bottom Line

More people are discovering the benefits of multigenerational living. For the best information and help deciding what’s right for your personal situation, let’s connect and start the conversation today.

Monday, November 14, 2022

Home Prices Rose Year-Over-Year in 98% of Metro Areas in Third Quarter of 2022

Home Prices Rose Year-Over-Year in 98% of Metro Areas in Third Quarter of 2022: The median income needed to buy a typical home has risen to $88,300, almost $40,000 more than it was prior to the start of the pandemic, in 2019.

Tuesday, October 25, 2022

Existing-Home Sales Decreased 1.5% in September

Existing-Home Sales Decreased 1.5% in September: Three out of the four major U.S. regions saw sales fall month-over-month, while the West held steady. Year-over-year, sales dropped in all regions.

Thursday, October 13, 2022

Perspective Matters When Selling Your House Today

Perspective Matters When Selling Your House Today

Does the latest news about the housing market have you questioning your plans to sell your house? If so, perspective is key. Here are some of the ways a trusted real estate professional can explain the shift that’s happening today and why it’s still a sellers’ market even during the cooldown.

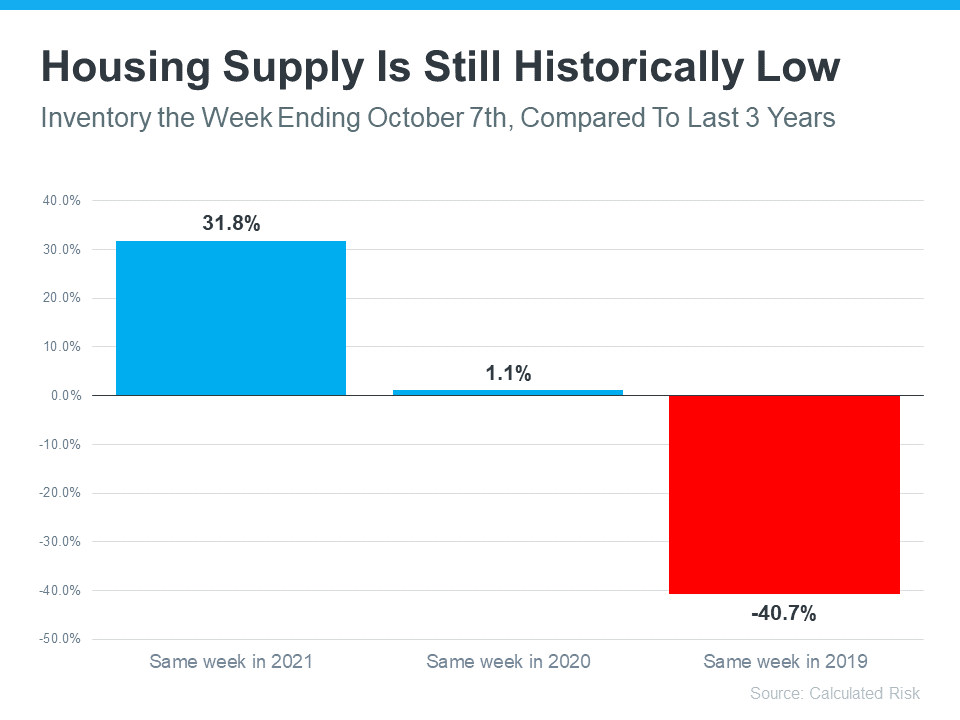

Fewer Homes for Sale than Pre-Pandemic

While the supply of homes available for sale has increased this year compared to last, we’re still nowhere near what’s considered a balanced market. A recent article from Calculated Risk helps put this year’s increased inventory into context (see graph below):

It shows supply this year has surpassed 2021 levels by over 30%. But the further back you look, the more you’ll understand the big picture. Compared to 2020, we’re just barely above the level of inventory we saw then. And if you go all the way back to 2019, the last normal year in real estate, we’re roughly 40% below the housing supply we had at that time.

Why does this matter to you? When inventory is low, there is still demand for your house because there just aren’t enough homes available for sale.

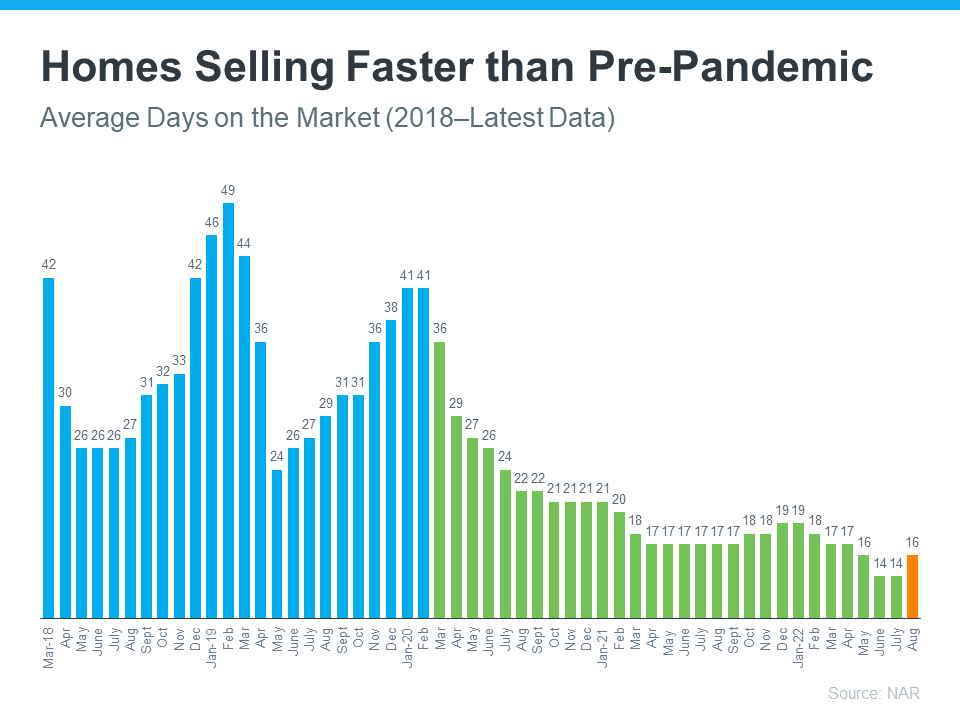

Homes Are Still Selling Faster Than More Normal Years

And while homes aren’t selling as quickly as they did a few months ago, the average number of days on the market is still well below pre-pandemic norms – in large part because inventory is so low. The graph below uses data from the Realtors’ Confidence Index by the National Association of Realtors (NAR) to illustrate this trend:

As the graph shows, the pre-pandemic numbers (shown in blue) are higher than the numbers we saw during the pandemic (shown in green). That’s because the average days on the market started to decrease as homes sold at record pace during the pandemic. Most recently, due to the cooldown in the housing market, the average days on the market have started to tick back up slightly (shown in orange) but are still far below the pre-pandemic norm.

What does this mean for you? While it may not be as fast as it was a couple of months ago, homes are still selling much faster than they did in more normal, pre-pandemic years. And if you price it right, your home could still go under contract quickly.

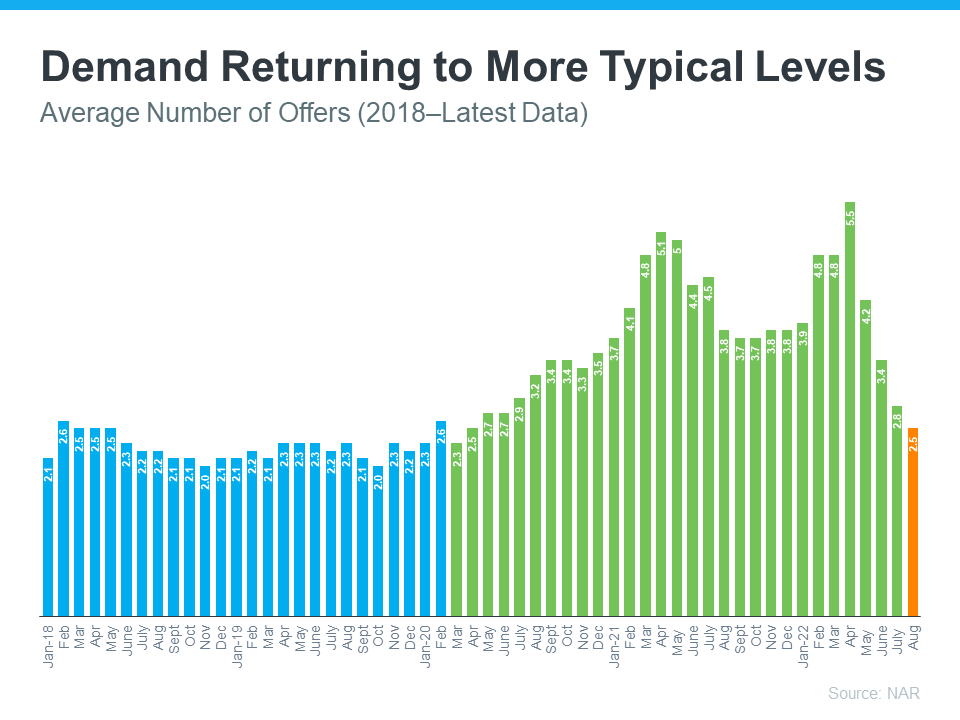

Buyer Demand Has Moderated and Is Now in Line with More Typical Years

Buyer demand has softened this year in response to rising mortgage rates. But again, perspective is key. Getting 3-5 offers like sellers did during the pandemic isn’t the norm. The graph below uses data from NAR going back to 2018 to help tell the story of this shift over time (see graph below):

Prior to the pandemic, it was typical for homes sold to see roughly 2-2.5 offers (shown in blue). As the market heated up during the pandemic, the average number of offers skyrocketed as record-low mortgage rates drove up demand (shown in green). But most recently, the number of offers on homes sold today (shown in orange) has started to return to pre-pandemic levels as the market cools from the frenzy.

What’s the takeaway for you? Buyer demand has moderated from the pandemic peak, but it hasn’t disappeared. The buyers are still out there, and if you price your house at current market value, you’ll still be able sell your house today.

Bottom Line

If you have questions about selling your house in today’s housing market, let’s connect. That way you have context around what’s happening now, so you’re up to date on what you can expect when you’re ready to move.

Tuesday, October 11, 2022

What Are Experts Saying About the Fall Housing Market?

What Are Experts Saying About the Fall Housing Market?

The housing market is rapidly changing from the peak frenzy it saw over the past two years. That means you probably have questions about what your best move is if you’re thinking of buying or selling this fall.

To help you make a confident decision, lean on the professionals for insights. Here are a few things experts are saying about the fall housing market.

Expert Quotes for Fall Homebuyers

A recent article from realtor.com:

“This fall, a more moderate pace of home selling, more listings to choose from, and softening price growth will provide some breathing room for buyers searching for a home during what is typically the best time to buy a home.”

Michael Lane, VP and General Manager, ShowingTime:

“Buyers will continue to see less competition for homes and have more time to tour homes they like and consider their options.”

Expert Quotes for Fall Sellers

Selma Hepp, Interim Lead of the Office of the Chief Economist, CoreLogic:

“. . . record equity continues to provide fuel for housing demand, particularly if households are relocating to more affordable areas.”

Danielle Hale, Chief Economist, realtor.com:

“For homeowners deciding whether to make a move this year, remember that listing prices – while lower than a few months ago – remain higher than in prior years, so you're still likely to find opportunities to cash-in on record-high levels of equity, particularly if you've owned your home for a longer period of time.”

Bottom Line

Mortgage rates, home prices, and the supply of homes for sale are top of mind for buyers and sellers today. And if you want the latest information for our area, let’s connect today.

Thursday, October 6, 2022

Pending Home Sales Dropped 2.0% in August

Pending Home Sales Dropped 2.0% in August: August 2022 pending home sales were down 2.0% from July, and contract signings fell year-over-year by double-digit percentages in each region of the U.S.

The True Strength of Homeowners Today

The True Strength of Homeowners Today

The real estate market is on just about everyone’s mind these days. That’s because the unsustainable market of the past two years is behind us, and the difference is being felt. The question now is, just how financially strong are homeowners throughout the country? Mortgage debt grew beyond 10 trillion dollars over the past year, and many called that a troubling sign when it happened for the first time in history.

Recently Odeta Kushi, Deputy Chief Economist at First American, answered that question when she said:

“U.S. households own $41 trillion in owner-occupied real estate, just over $12 trillion in debt, and the remaining ~$29 trillion in equity. The national "LTV" in Q2 2022 was 29.5%, the lowest since 1983.”

She continued on to say:

“Homeowners had an average of $320,000 in inflation-adjusted equity in their homes in Q2 2022, an all-time high.”

What Is LTV?

The term LTV refers to loan to value ratio. For more context, here’s how the Mortgage Reports defines it:

“Your ‘loan to value ratio’ (LTV) compares the size of your mortgage loan to the value of the home. For example: If your home is worth $200,000, and you have a mortgage for $180,000, your LTV ratio is 90% — because the loan makes up 90% of the total price.

You can also think about LTV in terms of your down payment. If you put 20% down, that means you’re borrowing 80% of the home’s value. So your LTV ratio is 80%.”

Why Is This Important?

This is yet another reason we won’t see the housing market crash. Home equity allows homeowners to be in control. For example, if someone did need to sell their home, they likely have the equity they need to be able to sell it and still put money in their pocket. This was not the case back in 2008, when many owed more on their homes than they were worth.

Bottom Line

Homeowners today have more financial strength than they have had since 1983. This is a combination of how homeowners have handled equity since the crash and rising home prices of the last two years. And this is yet another reason homeownership in any market makes sense.

Friday, September 30, 2022

Why Buying a Home May Make More Sense Than Renting [INFOGRAPHIC]

Why Buying a Home May Make More Sense Than Renting [INFOGRAPHIC]

![Why Buying a Home May Make More Sense Than Renting [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/09/29141015/20220930-MEM-1046x1845.png)

Some Highlights

- If you’re trying to decide whether to rent or buy a home, consider the advantages homeownership offers.

- Buying a home can help you escape the cycle of rising rents, it’s a powerful wealth-building tool, and it’s typically considered a good hedge against inflation.

- If you’re ready to take advantage of the benefits of homeownership, let’s connect to explore your options.

Wednesday, September 14, 2022

7 Most Popular Bathroom Upgrades

7 Most Popular Bathroom Upgrades: Homeowners are spending a median of $9,000 on bathroom renovations, which is 13% higher than last year, a new study finds. These are their favorite trends.

Tuesday, September 13, 2022

How Owning a Home Builds Your Net Worth

How Owning a Home Builds Your Net Worth

Owning a home is a major financial milestone and an achievement to take pride in. One major reason: the equity you build as a homeowner gives your net worth a big boost. And with high inflation right now, the link between owning your home and building your wealth is especially important.

If you’re looking to increase your financial security, here’s why now could be a good time to start on your journey toward homeownership.

Owning a Home Is a Key Ingredient for Financial Success

A report from the National Association of Realtors (NAR) details several homeownership trends, including a significant gap in net worth between homeowners and renters. It finds:

“. . . the net worth of a homeowner was about $300,000 while that of a renter’s was $8,000 in 2021.”

To put that into perspective, the average homeowner’s net worth is roughly 40 times that of a renter’s. This difference shows owning a home is a key step in achieving financial success.

Equity Gains Can Substantially Boost a Homeowner’s Net Worth

The net worth gap between owners and renters exists in large part because homeowners build equity. When you own a home, your equity grows as your home appreciates in value and you make your mortgage payments each month. As a renter, you don’t have that same opportunity. A recent article from CNET explains:

“Homeownership is still considered one of the most reliable ways to build wealth. When you make monthly mortgage payments, you're building equity in your home . . . When you rent, you aren't investing in your financial future the same way you are when you're paying off a mortgage.”

But on top of that, your home equity grows even more as your home appreciates in value over time. That has a major impact on the wealth you build, as a recent article from Bankrate notes:

“Building home equity can help you increase your wealth over time, . . . A home is one of the only assets that have the potential to appreciate in value as you pay it down.”

In other words, when you own your home, you have the advantage of your mortgage payment acting as a contribution to a forced savings account that grows in value as your home does. And when you sell, any equity you’ve built up comes back to you. As a renter, you’ll never see a return on the money you pay out in rent every month.

Bottom Line

Owning a home is an important part of building your net worth. If you’re ready to start on your journey to homeownership, let’s connect today.

Monday, September 12, 2022

Mortgage Rates Rise Again, Nearing Affordability Threshold

Mortgage Rates Rise Again, Nearing Affordability Threshold: If borrowing costs get just a little higher, the average household may be blocked from homeownership, warns an NAR economist.

Thursday, September 8, 2022

Should I Sell My House This Year?

Should I Sell My House This Year?

There’s no denying the housing market is undergoing a shift this season as buyer demand slows and the number of homes for sale grows. But that shift actually gives you some unique benefits when you sell. Here’s a look at the key opportunities you have if you list your house this fall.

Opportunity #1: You Have More Options for Your Move

One of the biggest stories today is the growing supply of homes for sale. Housing inventory has been increasing since the start of the year, primarily because higher mortgage rates helped cool off the peak frenzy of buyer demand. But what you may not realize is, that actually could benefit you.

If you’re selling your house to make a move, it means you’ll have more options for your own home search. That gives you an even better chance to find a home that checks all of your boxes. So, if you’ve put off selling because you were worried about being able to find somewhere to go, know your options have improved.

Opportunity #2: The Number of Homes on the Market Is Still Low

Just remember, while data shows the number of homes for sale has increased this year, housing supply is still firmly in sellers’ market territory. To be in a balanced market where there are enough homes available to meet the pace of buyer demand, there would need to be a six months’ supply of homes. According to the latest report from the National Association of Realtors (NAR), in July, there was only a 3.3 months’ supply.

While you’ll have more options for your own home search, inventory is still low, and that means your home will still be in demand if you price it right. That’s why the most recent data from NAR also shows the average home sold in July still saw multiple offers and sold in as little as 14 days.

Opportunity #3: Your Equity Has Grown by Record Amounts

The home price appreciation the market saw over the past few years has likely given your equity (and your net worth) a considerable boost. Danielle Hale, Chief Economist at realtor.com, explains:

“Home owners trying to decide if now is the time to list their home for sale are still in a good position in many markets across the country as a decade of rising home prices gives them a substantial equity cushion . . .”

If you’ve been holding off on selling because you’re worried about how rising prices will impact your next home search, rest assured your equity can help. It may be just what you need to cover a large portion (if not all) of the down payment on your next home.

Bottom Line

If you’re thinking about selling your house this season, let’s connect so you have the expert insights you need to make the best possible move today.

Subscribe to:

Comments (Atom)

Should You Wait for Lower Rates?

Should You Wait for Lower Rates? Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they t...

-

Pending Home Sales Jumped 6.1% in March : The solid rise in pending home sales implies a sizable build-up of potential home buyers, fueled b...

-

Pending Home Sales Waned 4.6% in January : The Midwest, South, and West saw month-over-month losses in transactions, while the Northeast saw...